Strengthening Nepal’s Non-Profit Sector: The Evolving AML Landscape...

An in-depth look at how Nepal is strengthening its AML...

8 minutes read Read MoreHYPERCHARGED SOLUTIONS FOR

We will deliver scalable, flexible and easy-to-use solutions to organizations of different sizes across the world, to meet their risk and compliance needs

About Us

We leverage our proprietary Integrated RegTech Stack to offer the Risk Application Ecosystem to customers across the world, to help manage risks and compliance driven use cases

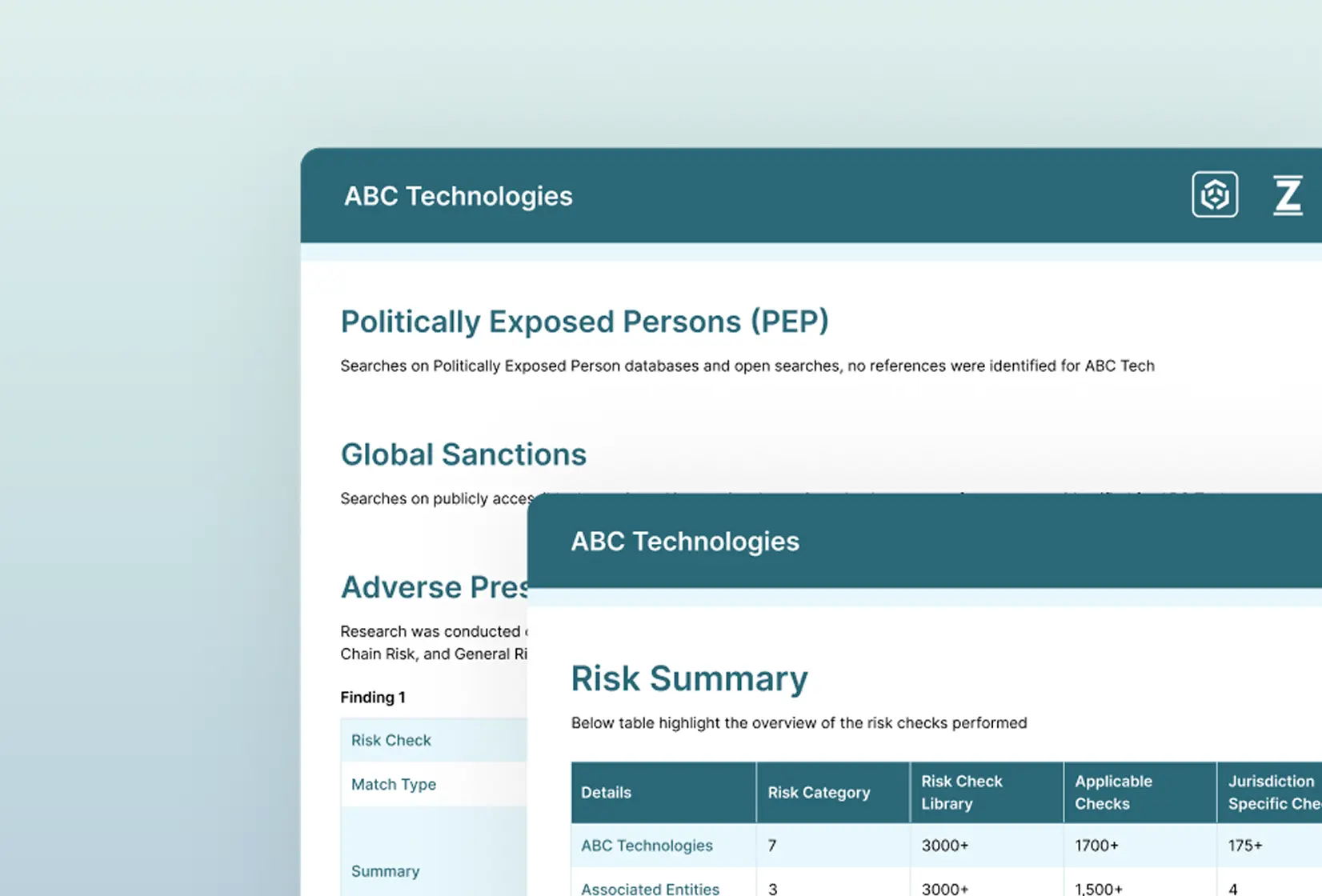

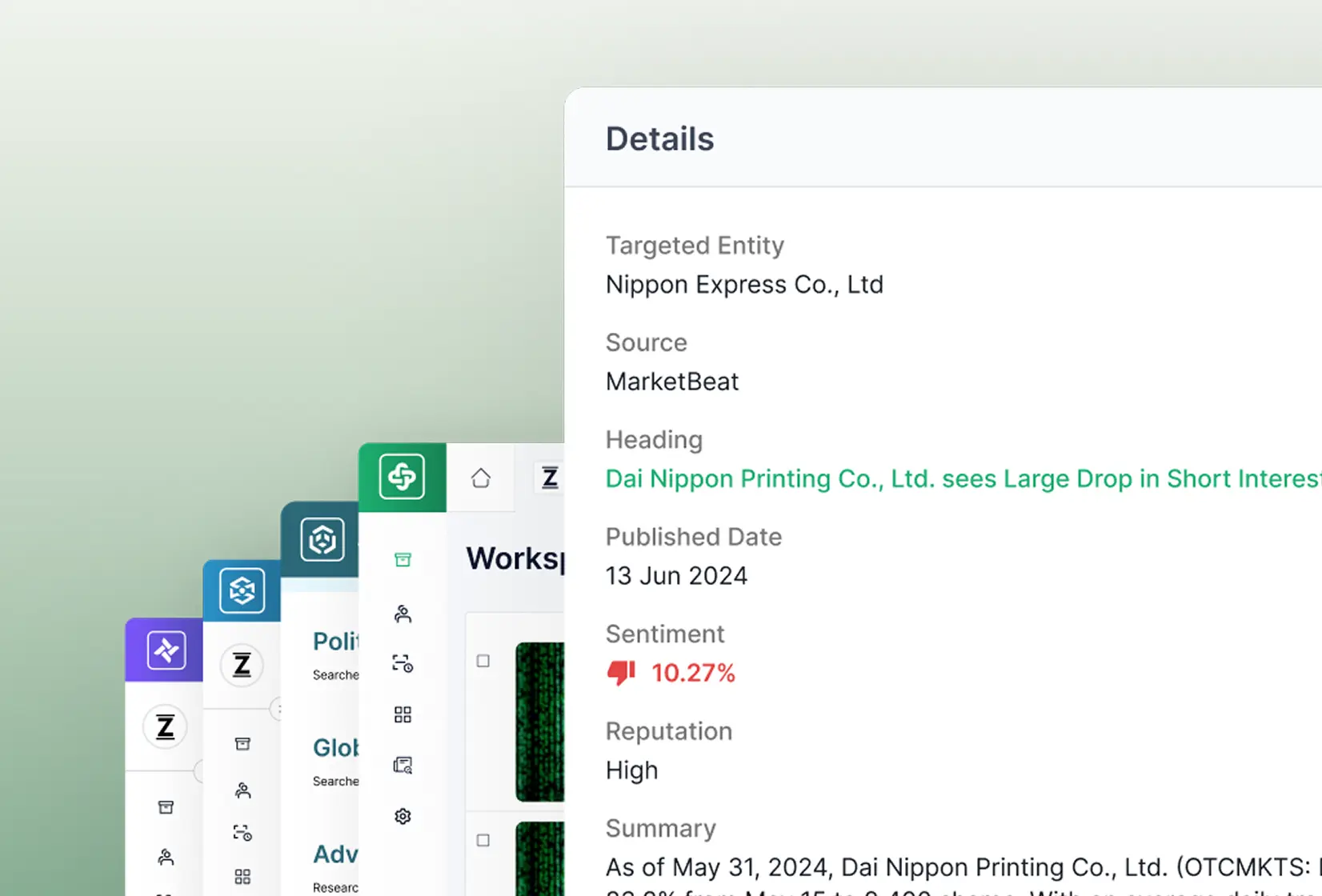

Research-driven due diligence reports to identify potential red flags

Learn More

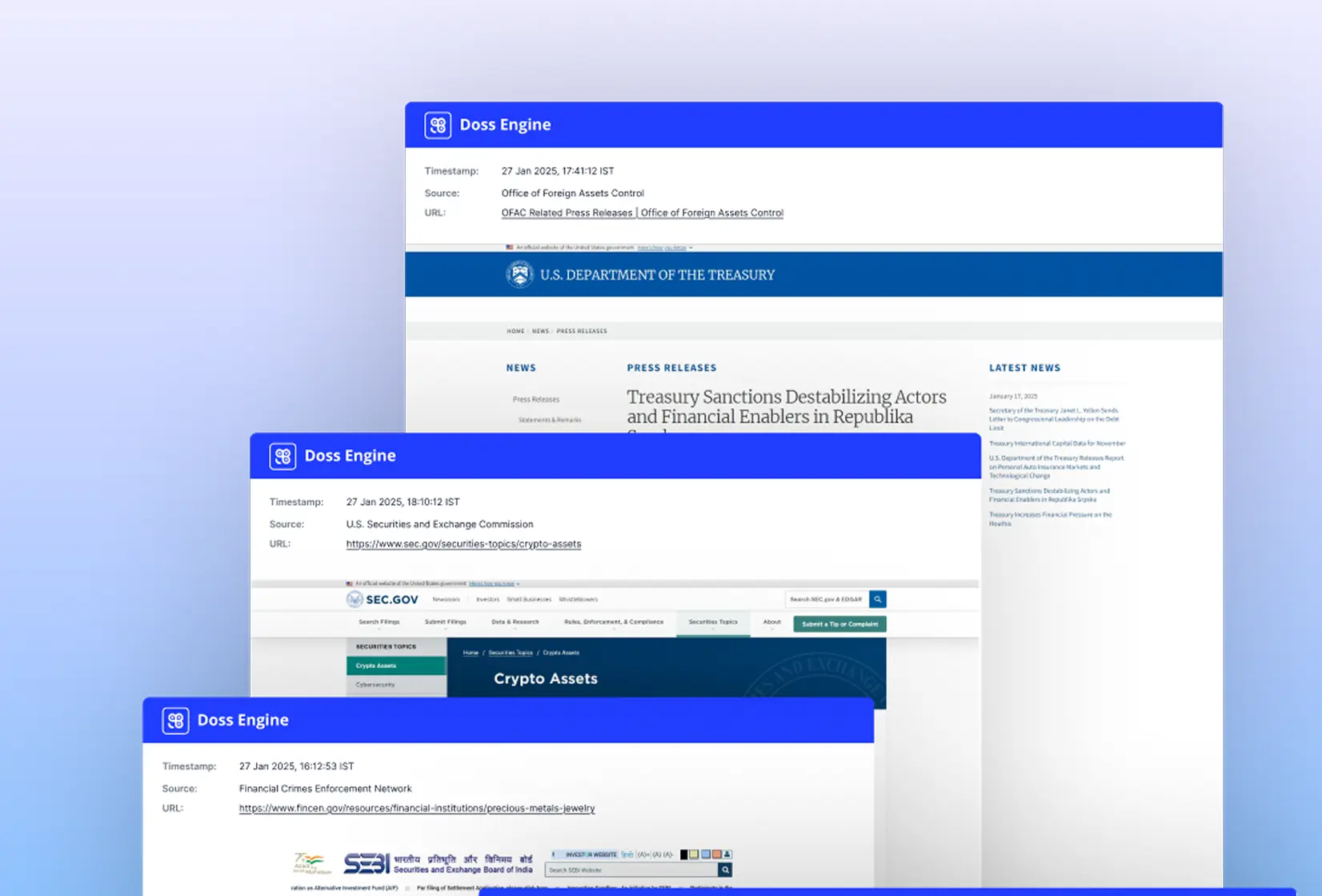

Intelligent online content monitoring application for enterprises

Learn More

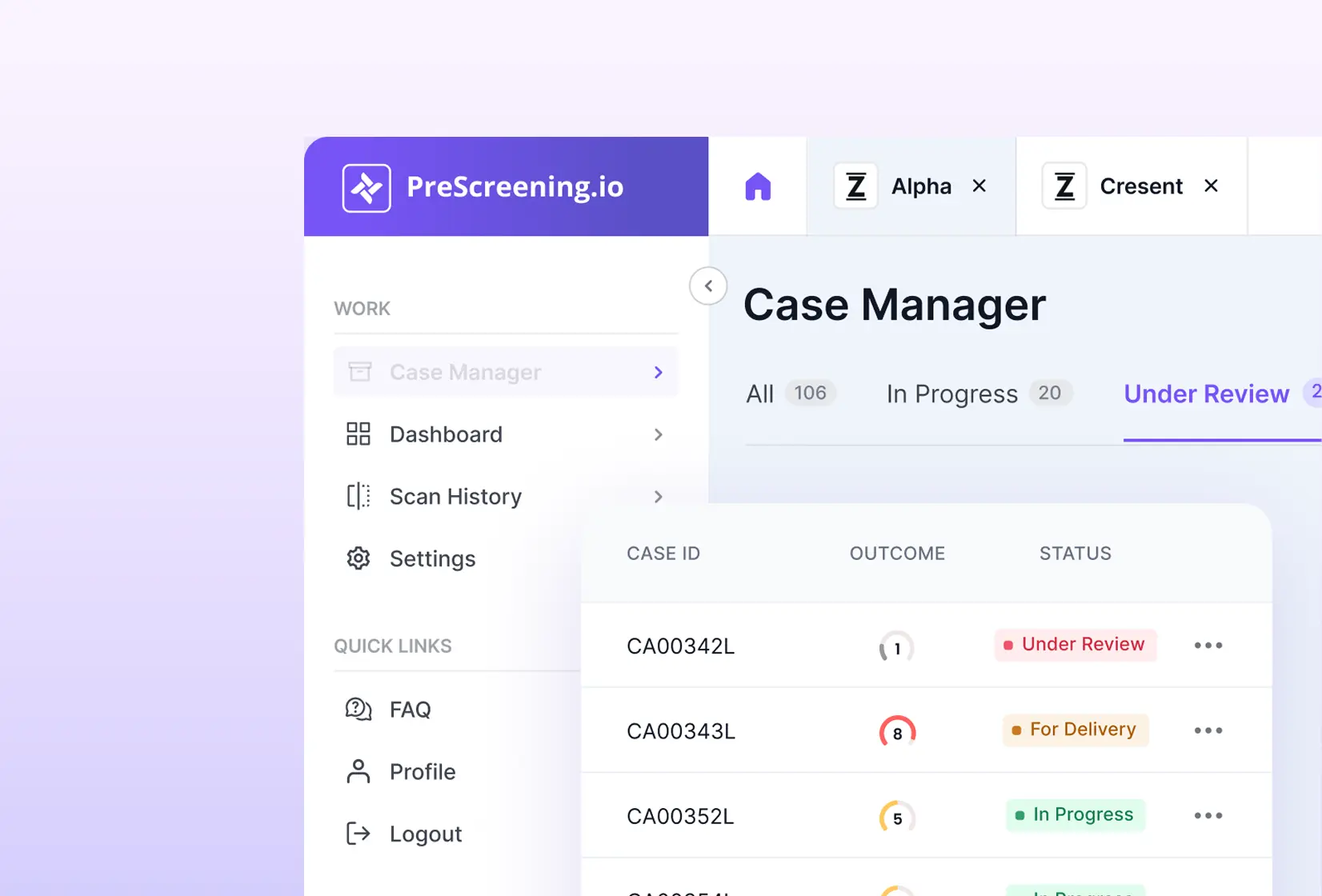

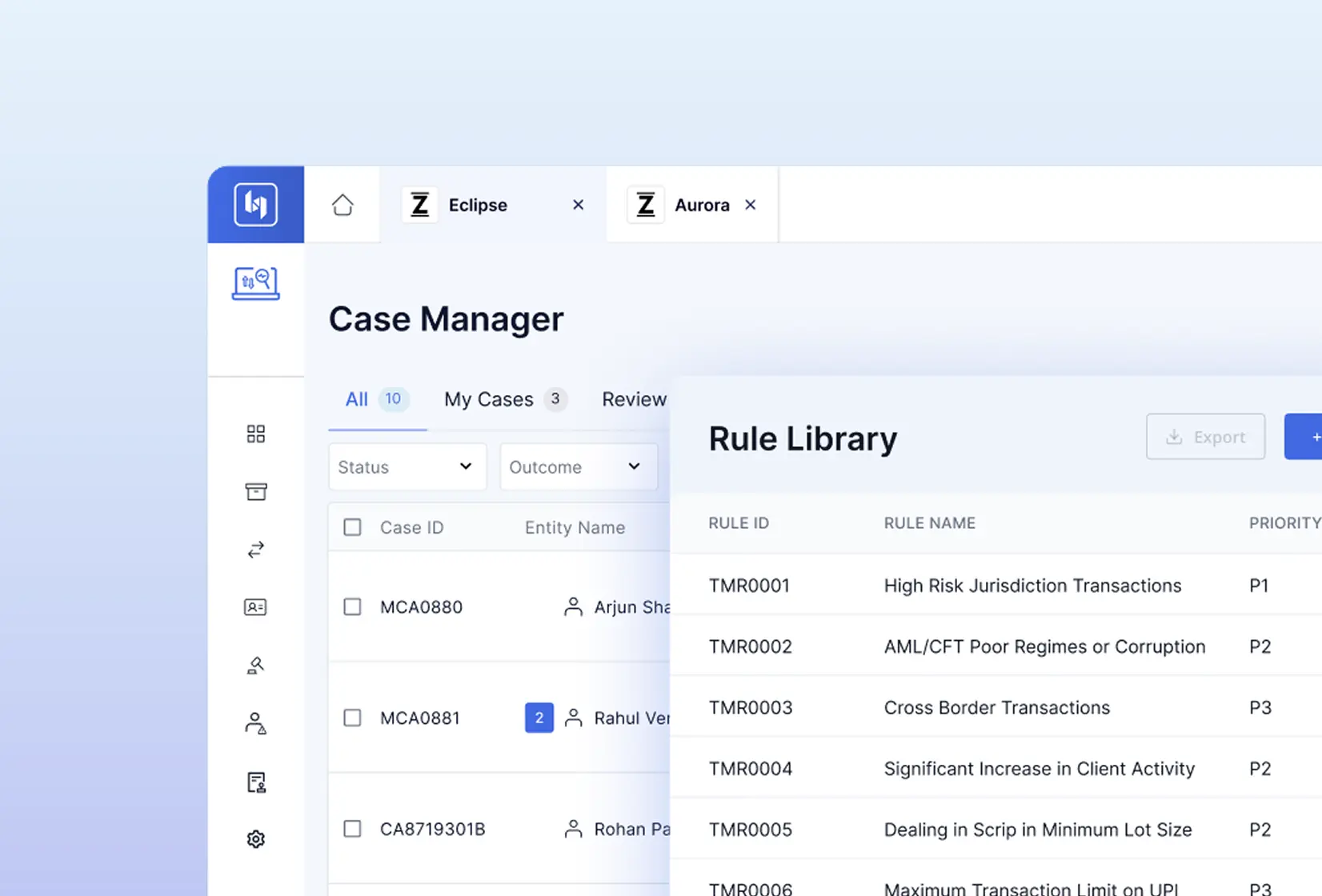

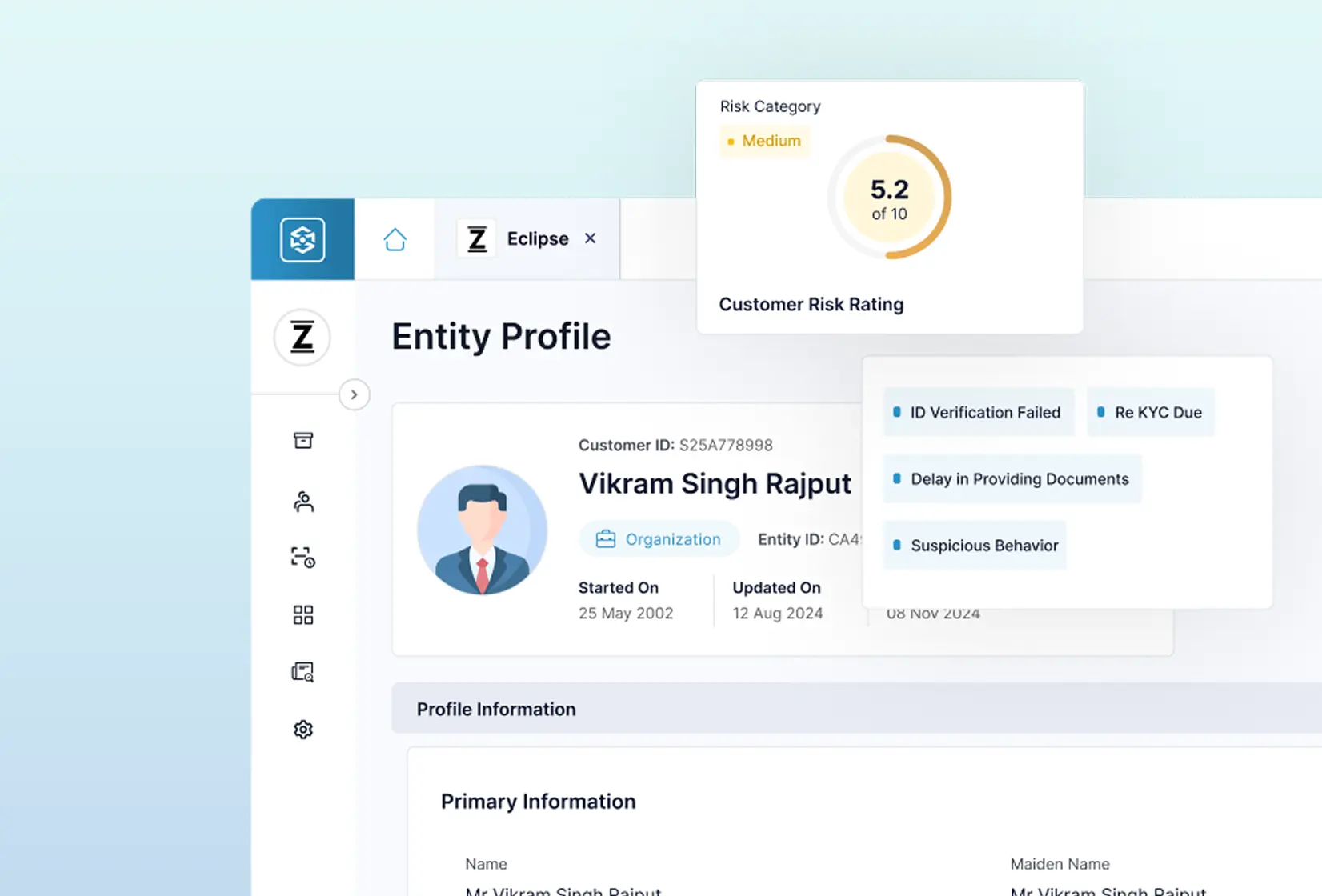

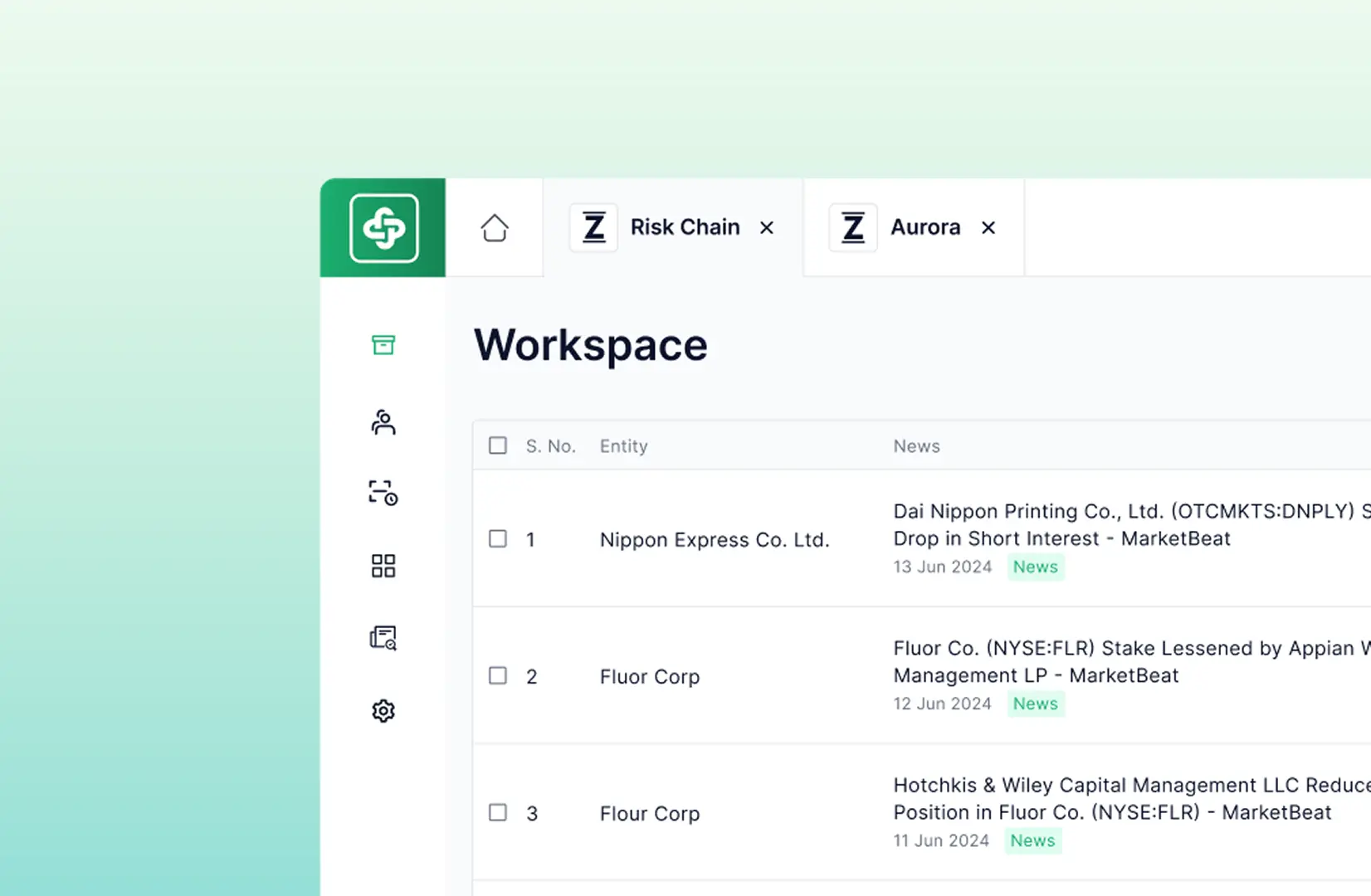

Anti Money Laundering (AML) & Financial Crimes Compliance (FCC) data platform

Learn MoreWe are a rapidly growing global data asset company with a fully integrated RegTech stack featuring proprietary data, cutting-edge applications, advanced intelligence, and comprehensive services.

Risk Use Cases

Professionals

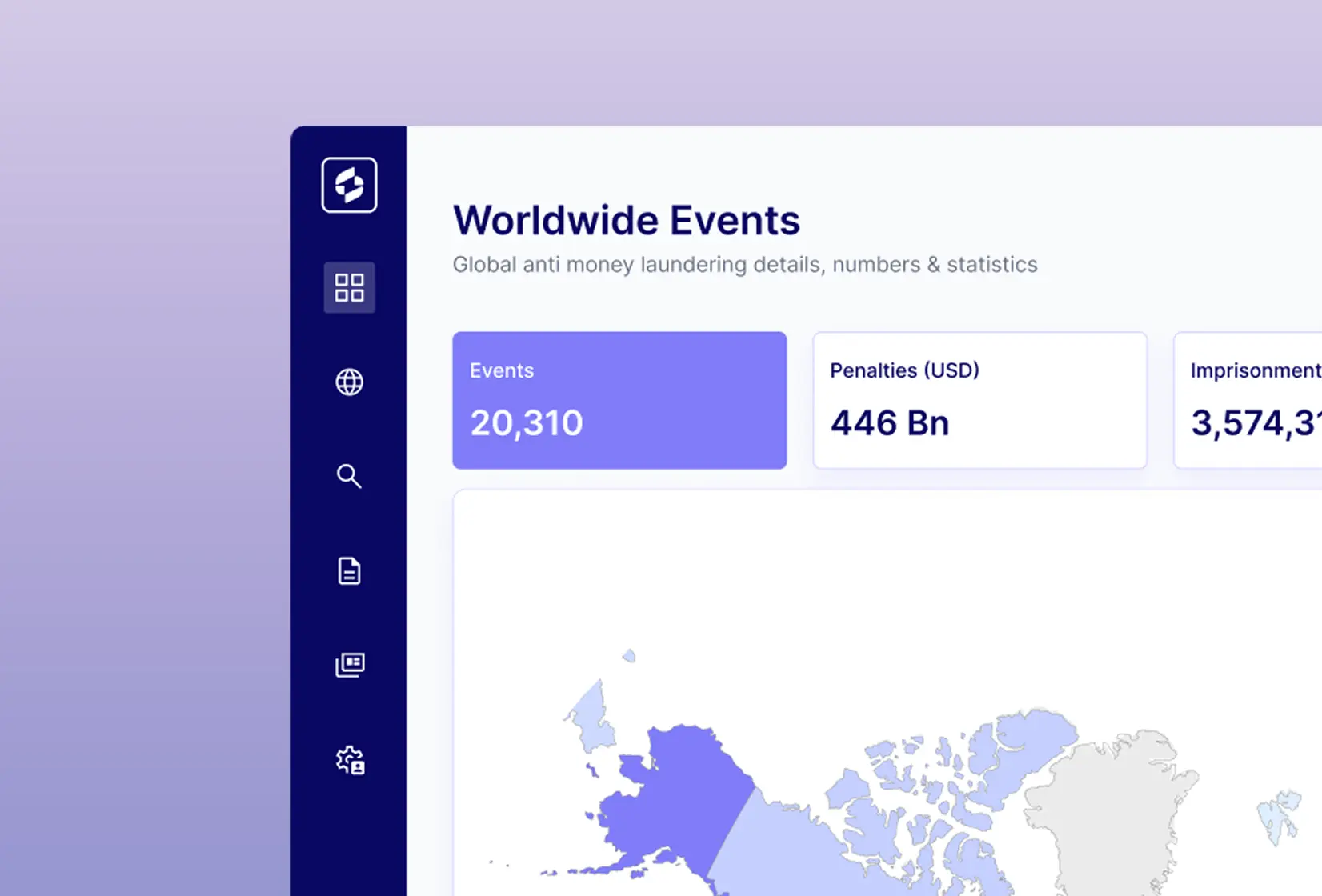

Billion Risk Scans

Deployments

Global Jurisdictions

Billion News Content

Watchlists

Languages

An in-depth look at how Nepal is strengthening its AML...

8 minutes read Read MoreAn in-depth analysis of beneficial ownership transparency reforms across British...

17 minutes read Read MoreRBI’s updated KYC FAQs clarify compliance routines, enable flexible onboarding,...

5 minutes read Read MoreAn in-depth look at how Saudi Arabia’s Capital Market Authority...

6 minutes read Read MoreExplore AML compliance in the UAE’s gold and precious metals...

18 minutes read Read MoreAn in-depth analysis of the UK’s Economic Crime and Corporate...

20 minutes read Read MoreOur weekly dose of knowledge on the latest developments in anti-money laundering, financial crime, and other offenses, including news, regulations, and reports from around the world

Weekly Anti Money Laundering News: A $245M Bitcoin thief faces...

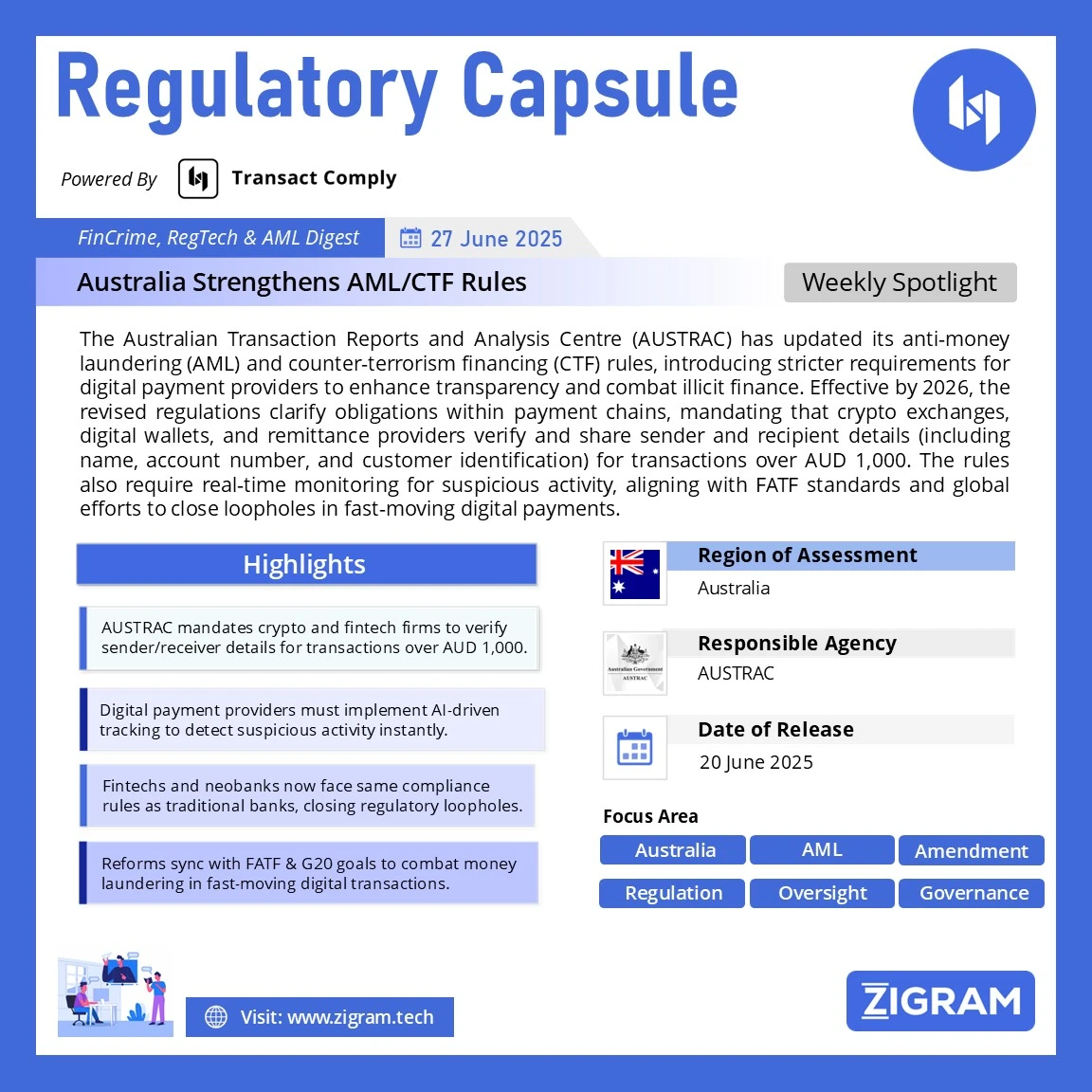

2 minutes read Read MoreThis week, we review the AML/CFT rules updated by AUSTRAC

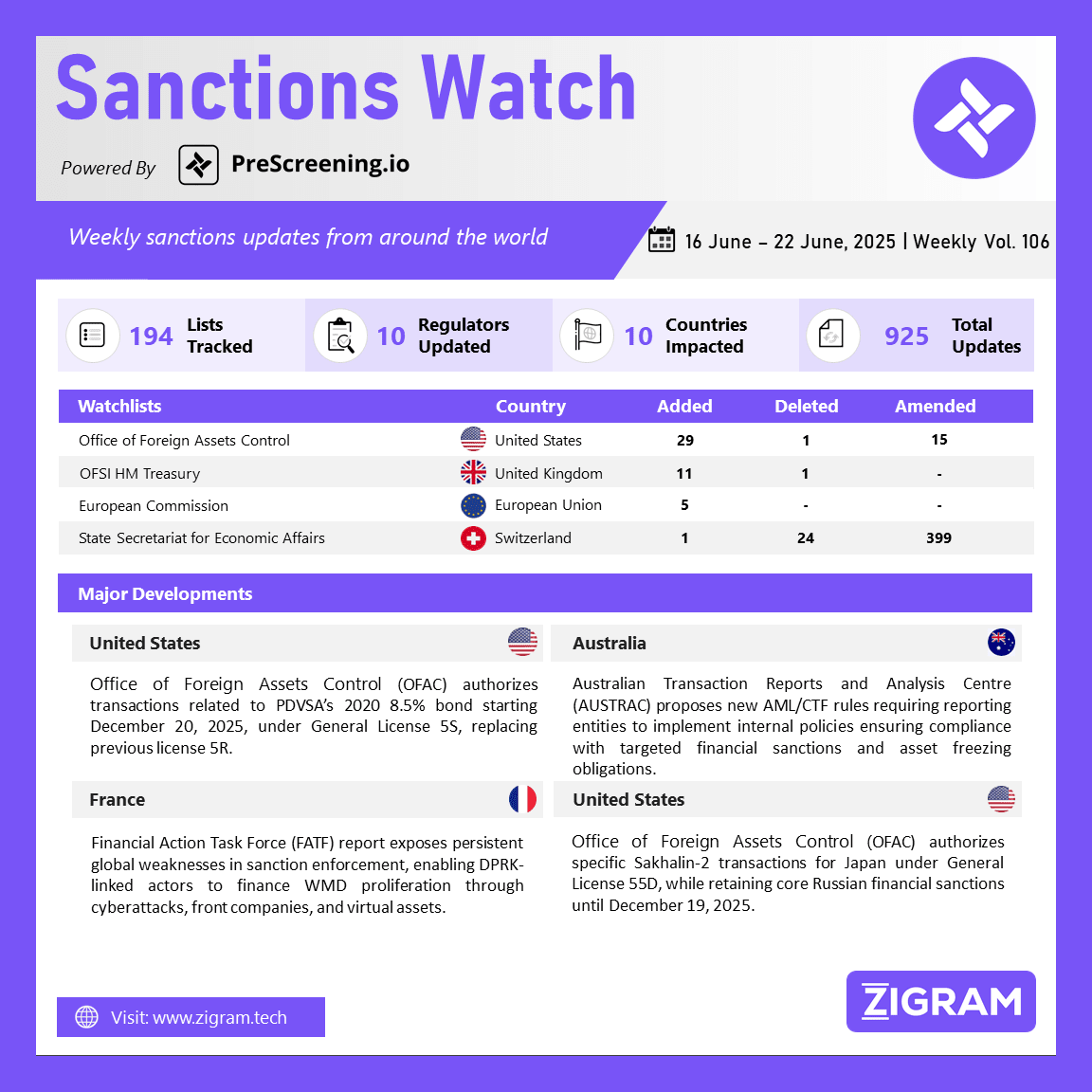

1 minutes read Read MoreOur 106th Sanctions Watch digest covers U.S. Treasury Issues General...

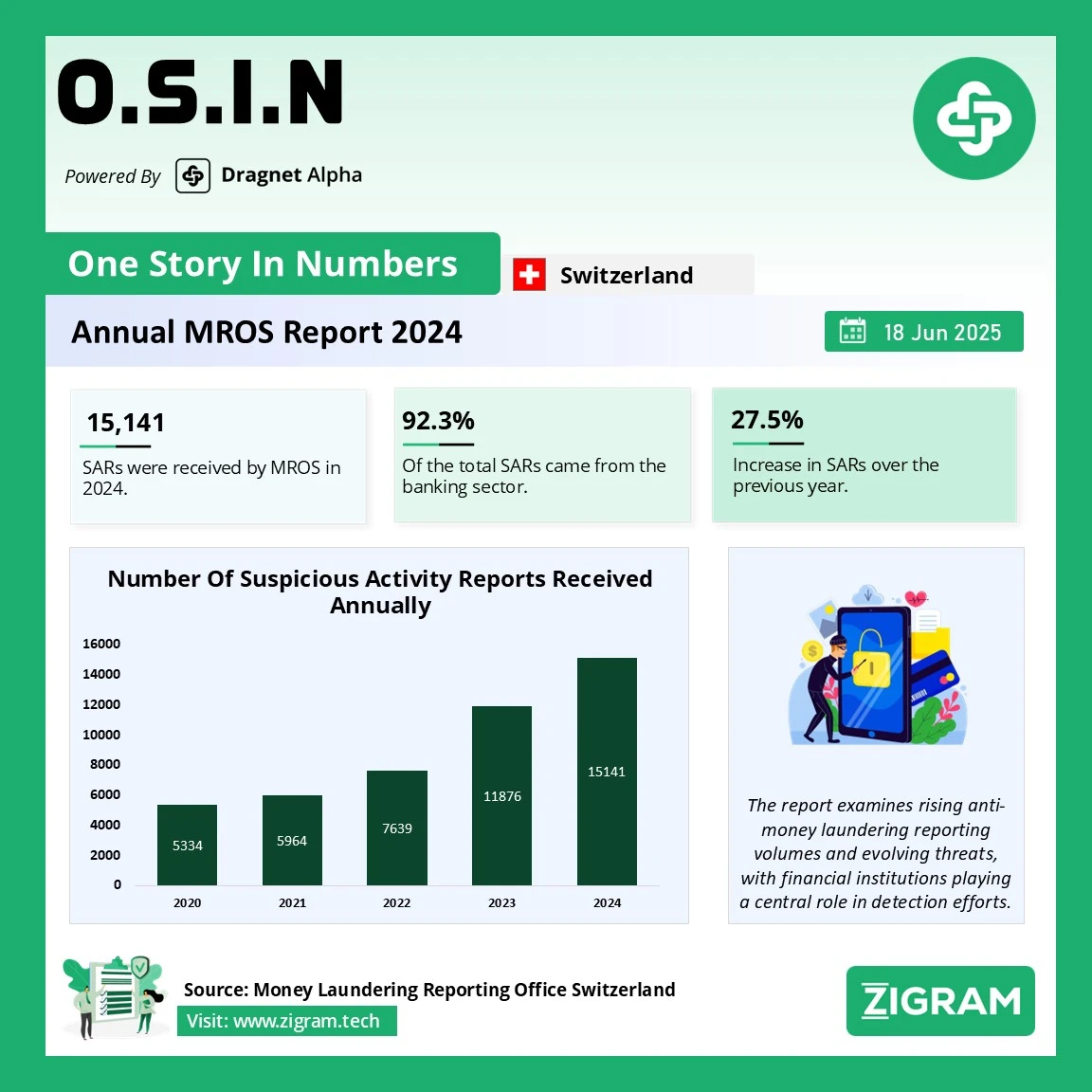

4 minutes read Read MoreIn this week's One Story In Number (OSIN), we review...

2 minutes read Read MoreWeekly Anti Money Laundering News: Singapore enforces strict crypto rules,...

4 minutes read Read More107th PEP Weekly Digest: Seyed Ali Madani-Zadeh Appointed Iran’s New...

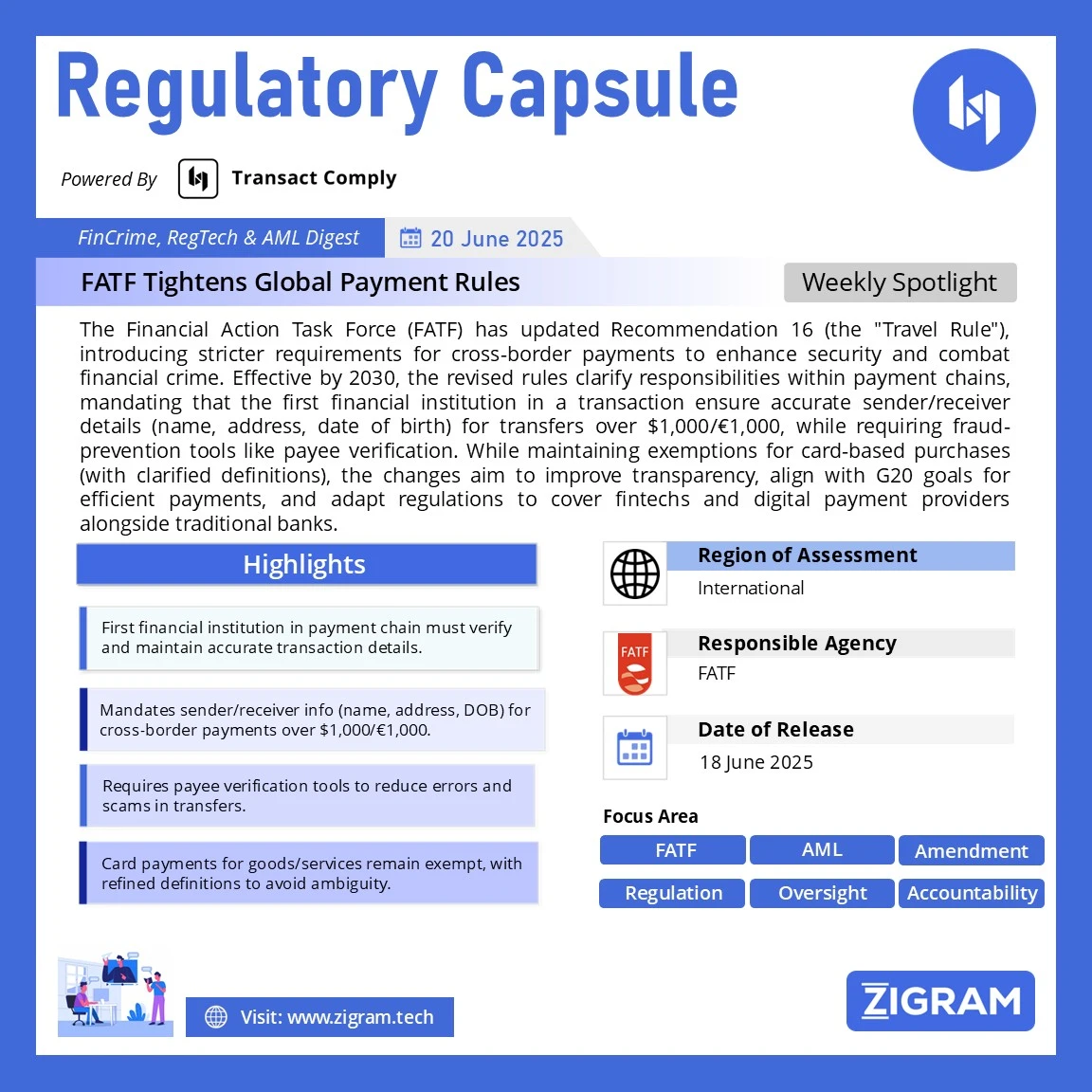

4 minutes read Read MoreThis week, we review the Recommendation 16 ("Travel Rule") changes...

2 minutes read Read MoreOur 105th Sanctions Watch digest covers OFAC Released Quarterly Licensing...

5 minutes read Read MoreIn this week's One Story In Number (OSIN), we review...

2 minutes read Read MoreLEARN MORE

Discover how our technology and data solutions can accelerate your compliance goals.

Copyright © 2025 ZIGRAM Data Technologies Pvt Ltd