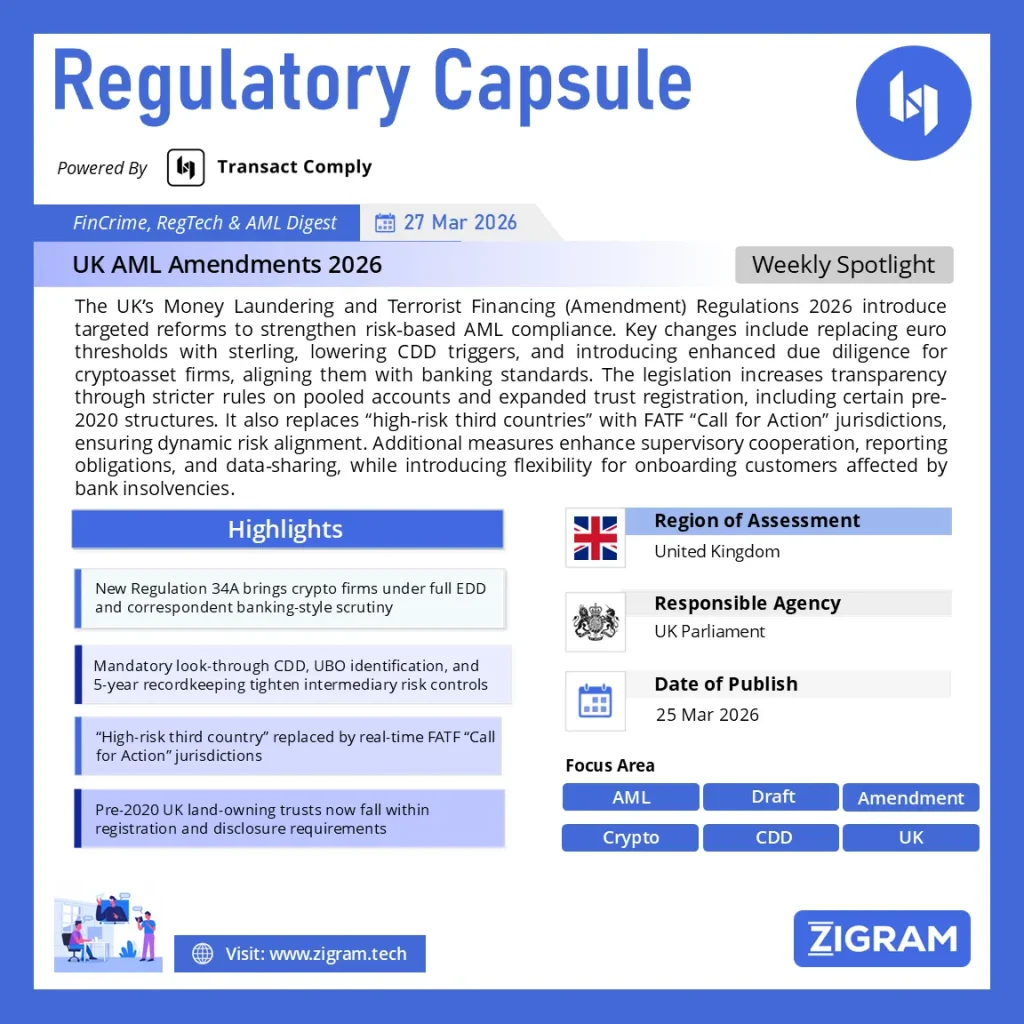

Regulation Name: Money Laundering and Terrorist Financing (Amendment) Regulations 2026

Date Of Issue: 25 Mar 2026

Region: United Kingdom

Agency: UK Parliament

UK AML Regulatory Overhaul 2026: Full Breakdown of Amendments to the MLR 2017

The Money Laundering and Terrorist Financing (Amendment) Regulations 2026 mark one of the most comprehensive upgrades to the UK’s AML/CFT framework since the 2017 MLRs.

This draft statutory instrument introduces targeted but high-impact amendments across:

- Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

- Cryptoasset regulation

- Trust transparency

- Supervisory cooperation and data-sharing

- Risk definitions aligned with FATF

- Operational flexibility for crisis scenarios (e.g., bank insolvencies)

For AML leaders, this is not incremental—it is a systemic recalibration toward risk precision, digital finance oversight, and enforcement readiness.

Here is a line-by-line regulatory change tracker tailored for AML compliance, legal, and implementation teams. It maps each amendment → what changed → what it means → what you must do.

Line-by-Line Regulatory Change Tracker (Implementation Ready)

PART 1: GENERAL & COMMENCEMENT

Regulation | Change | What It Means | Action Required |

Reg 1 | Staggered implementation (incl. crypto in 2027) | Phased compliance timelines | Build multi-phase implementation roadmap (2026 vs 2027 readiness) |

PART 2: CORE MLR 2017 AMENDMENTS

- DEFINITIONS & INTERPRETATION

Regulation | Change | Impact | Action |

Reg 3 | Introduces “cryptoasset business”; replaces € with £ | Aligns AML with UK + crypto scope | Update policy definitions, screening logic, thresholds |

- BUSINESS RELATIONSHIP SCOPE

Regulation | Change | Impact | Action |

Reg 4 | Adds new services (incl. off-the-shelf firms) | Expands onboarding scope | Update CDD triggers for TCSP clients |

- APPLICATION & COVERAGE

Regulation | Change | Impact | Action |

Reg 8 | Pooled accounts brought into AML scope | New risk category | Identify all pooled accounts across business lines |

- SECTOR-SPECIFIC SCOPE CHANGES

Regulation | Change | Impact | Action |

Reg 10 | Excludes reinsurance | Narrows AML scope slightly | Update product classification logic |

Reg 12 | Adds “off-the-shelf firm” definition | Targets shell structures | Enhance UBO + company lifecycle checks |

Reg 13–14 | €10k → £10k thresholds | Currency shift | Update transaction monitoring rules |

- EXCLUSIONS

Regulation | Change | Impact | Action |

Reg 15 | Expands exclusions + £1,000 threshold | Minor scope recalibration | Review exemption logic |

- RISK LANGUAGE MODIFICATION

Regulation | Change | Impact | Action |

Reg 19 & 19A | “Unusually complex or unusually large given nature” | Contextual risk-based AML | Re-tune scenario models & alerts |

- FCA REPORTING OBLIGATIONS

Regulation | Change | Impact | Action |

Reg 23 | Mandatory update within 30 days for changes/inaccuracies | Continuous compliance | Build regulatory reporting workflows + alerts |

CUSTOMER DUE DILIGENCE (CDD)

- THRESHOLDS & TRIGGERS

Regulation | Change | Impact | Action |

Reg 27 | €1,000 → £800; other threshold updates | More transactions captured | Adjust CDD trigger engines + onboarding rules |

- POOLED ACCOUNTS (MAJOR CHANGE)

Regulation | Change | Impact | Action |

Reg 29 | Full CDD + risk assessment + recordkeeping for pooled accounts | High-risk intermediary structures now transparent | |

Must identify underlying clients + UBOs | Removes opacity layer | Build look-through capability | |

5-year recordkeeping requirement | Audit trail enforcement | Enhance data retention systems | |

Law enforcement access mandatory | Increased disclosure obligations | Create rapid response workflows |

- SIMPLIFIED DUE DILIGENCE

Regulation | Change | Impact | Action |

Reg 37 | SDD linked with pooled account controls | SDD becomes conditional | Re-define low-risk classification logic |

TIMING & EXCEPTIONS

- INSOLVENT BANK CUSTOMERS (NEW REGIME)

Regulation | Change | Impact | Action |

Reg 30ZA (new) | Allows onboarding before full CDD | Crisis flexibility | Create exception onboarding workflows |

Reg 30 & 30A | Delay verification + discrepancy reporting | Reduced friction during insolvency events | Add scenario-based compliance playbooks |

ENHANCED DUE DILIGENCE (EDD)

- FATF ALIGNMENT

Regulation | Change | Impact | Action |

Reg 33 | “High-risk third country” → FATF Call for Action | Dynamic risk lists | Integrate real-time FATF list feeds |

- CRYPTO CORRESPONDENT EDD (CRITICAL)

Regulation | Change | Impact | Action |

Reg 34A (new) | Full EDD for crypto correspondent relationships | Crypto = banking-level scrutiny | |

Requires: reputation checks, AML controls, senior approval | Governance upgrade | Implement crypto onboarding frameworks | |

Prohibits shell bank exposure | High-risk restriction | Add counterparty screening rules | |

Requires downstream CDD assurance | Indirect risk visibility | Build KYCC (Know Your Customer’s Customer) capability |

ELECTRONIC MONEY & CRYPTO TRANSFERS

- THRESHOLD ADJUSTMENTS

Regulation | Change | Impact | Action |

Reg 38 | € thresholds → £150 / £50 | Minor adjustment | Update e-money monitoring rules |

Reg 64C / 64G | Crypto transfer threshold → £800 | Travel Rule tightening | Update crypto transaction monitoring |

TRUST TRANSPARENCY

- TRUST REGISTRATION EXPANSION

Regulation | Change | Impact | Action |

Reg 42, 45, 45ZA | Pre-2020 land-owning trusts now in scope | Backdated transparency | Conduct retrospective trust reviews |

New deadlines (e.g., Sept 2027) | Compliance window | Build remediation plan |

- TRUST ACCESS & CLASSIFICATION

Regulation | Change | Impact | Action |

Reg 45ZB | Adds Type C trusts | Broader access | Update data access controls |

- EXCLUDED TRUSTS EXPANSION

Regulation | Change | Impact | Action |

Schedule 3A | Low-value + temporary trusts excluded | Reduced burden | Reclassify low-risk trusts |

SUPERVISION & DATA SHARING

- REGULATORY COOPERATION

Regulation | Change | Impact | Action |

Reg 50 | Adds Companies House (Registrar) | Stronger corporate transparency | Integrate Companies House data feeds |

- DISCLOSURE EXPANSION

Regulation | Change | Impact | Action |

Reg 52 | Adds Financial Services Act investigator | Broader intelligence sharing | Update data-sharing policies |

- CONFIDENTIALITY FRAMEWORK

Regulation | Change | Impact | Action |

Reg 52A | Extends to crypto firms + aligns with FSMA | Crypto under full AML secrecy regime | Update confidentiality policies |

Reg 52B | Easier defence (either condition sufficient) | Legal risk recalibration | Update legal advisory frameworks |

CRYPTO REGULATORY TRANSFORMATION

- CHANGE IN CONTROL (SCHEDULE 6B)

Area | Change | Impact | Action |

Ownership thresholds | ≥10%, 20%, 30%, 50% triggers | Formal control regime | Build ownership monitoring systems |

FSMA alignment | Crypto treated like regulated firms | Regulatory parity | Align governance frameworks |

FCA oversight | Mandatory notifications | Increased scrutiny | Create regulatory notification workflows |

Criminal liability | Non-compliance penalties | Enforcement risk | Strengthen compliance controls |

PRIMARY LEGISLATION AMENDMENTS

- TERRORISM ACT 2000 & POCA 2002

Change | Impact | Action |

Currency updates (€ → £) | Consistency across AML laws | Align enterprise-wide thresholds |

Off-the-shelf firms included | Corporate misuse prevention | Enhance corporate onboarding checks |

FINAL IMPLEMENTATION PRIORITIES (FOR TEAMS)

Immediate (0–3 Months)

- Threshold updates (£ conversions)

- FATF list integration

- FCA reporting workflows

- Policy updates (definitions, crypto inclusion)

Medium-Term (3–9 Months)

- Pooled account frameworks

- Trust registration remediation

- Enhanced transaction monitoring recalibration

Long-Term (2027 Readiness)

- Crypto correspondent EDD

- Change-in-control governance (Schedule 6B)

- KYCC and network analytics capabilities

Bottom Line for AML Leaders

This is not just a regulatory update—it is an operational transformation blueprint:

- CDD → Contextual & deeper

- Crypto → Fully regulated

- Transparency → Expanded across trusts & accounts

- Supervision → Data-driven and interconnected

Detailed Explanation

Part 1: Foundational Structural Changes

- Legal Basis and Scope Expansion

The regulation is introduced under the Sanctions and Anti-Money Laundering Act 2018, reinforcing its alignment with UK sanctions and global AML frameworks.

Key Implementation Timelines:

- General provisions: 21 days post-enactment

- Crypto EDD (Regulation 34A): 1 February 2027

- Crypto control regime (Schedule 6B): phased until October 2027

Strategic Insight:

This staggered rollout signals regulatory prioritisation of crypto oversight while allowing institutions time to adapt.

Part 2: Core Amendments to the MLR 2017

- Currency Standardisation: Euro → Sterling Shift

A major structural change replaces euro-denominated thresholds with sterling equivalents (1:1 conversion) across the regime.

Examples:

- €10,000 → £10,000

- €1,000 → £800 (risk-calibrated adjustment in some cases)

Why It Matters:

- Aligns with post-Brexit regulatory independence

- Ensures FATF compliance while recalibrating thresholds to UK risk context

- Expansion of Scope: “Off-the-Shelf Firms”

Amendment:

Trust or Company Service Providers (TCSPs) now explicitly include:

- Selling off-the-shelf firms (inactive or minimally active companies)

Risk Impact:

- Addresses shell company misuse

- Closes loopholes in corporate structuring for ML/TF

- Clarification of Complex Transactions

Language updated from:

- “complex or unusually large” →

- “unusually complex or unusually large given the nature of the transaction”

Impact:

- Introduces contextual risk assessment

- Forces institutions to adopt risk-based, not rule-based monitoring

Part 3: Customer Due Diligence (CDD) Overhaul

- Revised CDD Thresholds

Key Changes:

- Occasional transaction threshold reduced: €1,000 → £800

- Other thresholds aligned to £12,000 / £10,000 depending on use case

Implication:

- More transactions fall under CDD scope

- Increased operational burden but improved detection

- Pooled Accounts: New AML Risk Category

New Requirements (Regulation 29):

Financial institutions must:

- Understand purpose and usage

- Verify consistency with customer risk profile

- Apply risk-based controls

- Maintain auditability and documentation

Customers must:

- Provide beneficial ownership details

- Maintain 5-year transaction records

- Share data with law enforcement upon request

Strategic Insight:

This is a major shift toward transparency in intermediary structures (e.g., law firms, brokers).

- Simplified Due Diligence (SDD) Recalibration

SDD now explicitly incorporates:

- Pooled account risk considerations

Impact:

SDD is no longer “light-touch”—it becomes risk-adjusted simplification.

Part 4: Crisis-Based Flexibility – Insolvent Bank Customers

- Introduction of Regulation 30ZA

A completely new framework allows:

- Account opening before full CDD completion for customers of failed banks

- Mandatory:

- Identity verification upfront

- Full CDD as soon as practicable

Safeguards:

- Transactions restricted if risk triggers emerge

- Applies only within 30 days of insolvency event

Strategic Value:

Balances:

- Financial stability

- AML risk control

Part 5: Redefining High-Risk Jurisdictions

- “High-Risk Third Country” → FATF Call for Action

Key Change:

- UK now directly references FATF “Call for Action” list

Why It Matters:

- Moves from static lists → dynamic global alignment

- Ensures real-time AML responsiveness

Part 6: Cryptoasset Regulation – The Biggest Shift

- New Regulation 34A: Crypto Correspondent EDD

Applies to:

- Crypto exchanges

- Custodian wallet providers

Mandatory Measures:

- Full due diligence on counterparties

- Reputation and supervision assessment

- Senior management approval

- Documented responsibilities

- Verification of downstream customers

Prohibitions:

- No relationships with shell banks

- No indirect exposure to shell bank usage

Strategic Impact:

This aligns crypto with:

- Traditional correspondent banking standards (FATF Rec 13)

- Technology risk controls (FATF Rec 15)

- Crypto Ownership & Control (Schedule 6B Overhaul)

Major Changes:

- Applies FSMA-style control thresholds to crypto firms:

- ≥10% ownership

- Voting power thresholds

- Significant influence

Introduces:

- Mandatory notification of control changes

- Fit-and-proper tests

- Criminal liability for non-compliance

Strategic Insight:

Crypto is no longer “lightly supervised”—it is entering full financial regulatory parity.

Part 7: Trust Transparency Expansion

- Expanded Trust Registration Requirements

Now includes:

- Trusts holding UK land before Oct 2020 and still active

Additional Changes:

- Expanded categories (Type C trusts)

- Removal of SDRT trigger for registration

- New deadlines (e.g., Sept 2027)

- Expansion of Excluded Trusts

New exclusions include:

- Low-value trusts (<£2,000 assets, <£5,000 income)

- Temporary post-death structures

- Estate variation trusts

Impact:

- Reduces administrative burden

- Focuses compliance on material risk structures

Part 8: Supervisory Cooperation & Data Sharing

- Inclusion of Companies House (Registrar)

Regulation 50 now includes:

- Registrar of Companies in AML cooperation framework

Implication:

- Stronger corporate transparency enforcement

- Integration with beneficial ownership data

- Expanded Disclosure Gateways

- Inclusion of Financial Services Act investigators

- Enhanced FCA information-sharing powers

- Confidentiality Framework Expanded

Now applies to:

- Cryptoasset businesses alongside banks

Also:

- Aligns with FSMA disclosure provisions

- Loosens criminal defence requirements (either condition sufficient)

Part 9: Reporting, Accuracy & Governance

- Mandatory Updates to FCA

Firms must:

- Report material changes or inaccuracies within 30 days

Impact:

- Continuous compliance obligation

- Reduces stale regulatory data risk

Part 10: Miscellaneous but High-Impact Changes

- Insurance Scope Narrowing

- Reinsurance excluded from AML scope

- Electronic Money Threshold Adjustments

- £150 / £50 limits updated

- Crypto Travel Rule Adjustments

- Thresholds aligned to £800

- Professional Body Update

- Updated supervisory authority list

Global AML Implications

This legislation positions the UK as:

- A leader in crypto AML regulation

- A pioneer in dynamic FATF alignment

- A driver of data-sharing-based compliance ecosystems

Global Ripple Effects:

- Multinational firms must harmonise UK AML with EU + FATF frameworks

- Crypto firms face global standardisation pressure

Key Strategic Takeaways for AML Leaders

- Risk-Based Compliance is Now Enforced

Static thresholds are replaced with contextual judgement requirements

- Crypto is Fully Mainstreamed into AML

Expect:

- Bank-level scrutiny

- Regulatory parity

- Transparency is Expanding Rapidly

Focus areas:

- Trusts

- Beneficial ownership

- Pooled accounts

- Supervisory Integration is Deepening

Data-sharing is no longer optional—it is structural

Conclusion

The UK AML Amendment Regulations 2026 represent a precision upgrade rather than a wholesale rewrite—but their impact is profound.

They:

- Close structural loopholes

- Strengthen enforcement readiness

- Integrate crypto into core AML

- Shift compliance toward intelligence and accountability

For AML professionals, the message is clear:

The future of compliance is real-time, risk-based, and deeply interconnected.

Read about the amendments here.

Read about the product: Transact Comply

Empower your organization with ZIGRAM’s integrated RegTech solutions – Book a Demo

- #AML

- #UKRegulation

- #FinancialCrime

- #CryptoAML

- #CDD

- #EDD

- #FATF

- #RegTech

- #Compliance

- #RiskManagement

- #TrustTransparency

- #KYC

- #FinCrime

- #AML2026

- #CryptoRegulation