Fraud Strategy 2026–2029: What AML Leaders Must Know About the UK’s System-Wide Crackdown on Fraud

Fraud is no longer just a financial crime issue—it is now a national security threat, economic disruptor, and systemic risk. The UK Government’s Fraud Strategy 2026–2029 represents one of the most comprehensive anti-fraud frameworks globally, combining regulatory reform, public-private collaboration, and technological intervention.

For AML compliance leaders, this strategy signals a fundamental shift from reactive compliance to proactive fraud prevention ecosystems.

The Scale of the Fraud Crisis: A Systemic Threat

The report highlights the unprecedented scale of fraud in the UK, underscoring why financial institutions must rethink AML frameworks.

- Fraud is the largest reported crime category in England and Wales

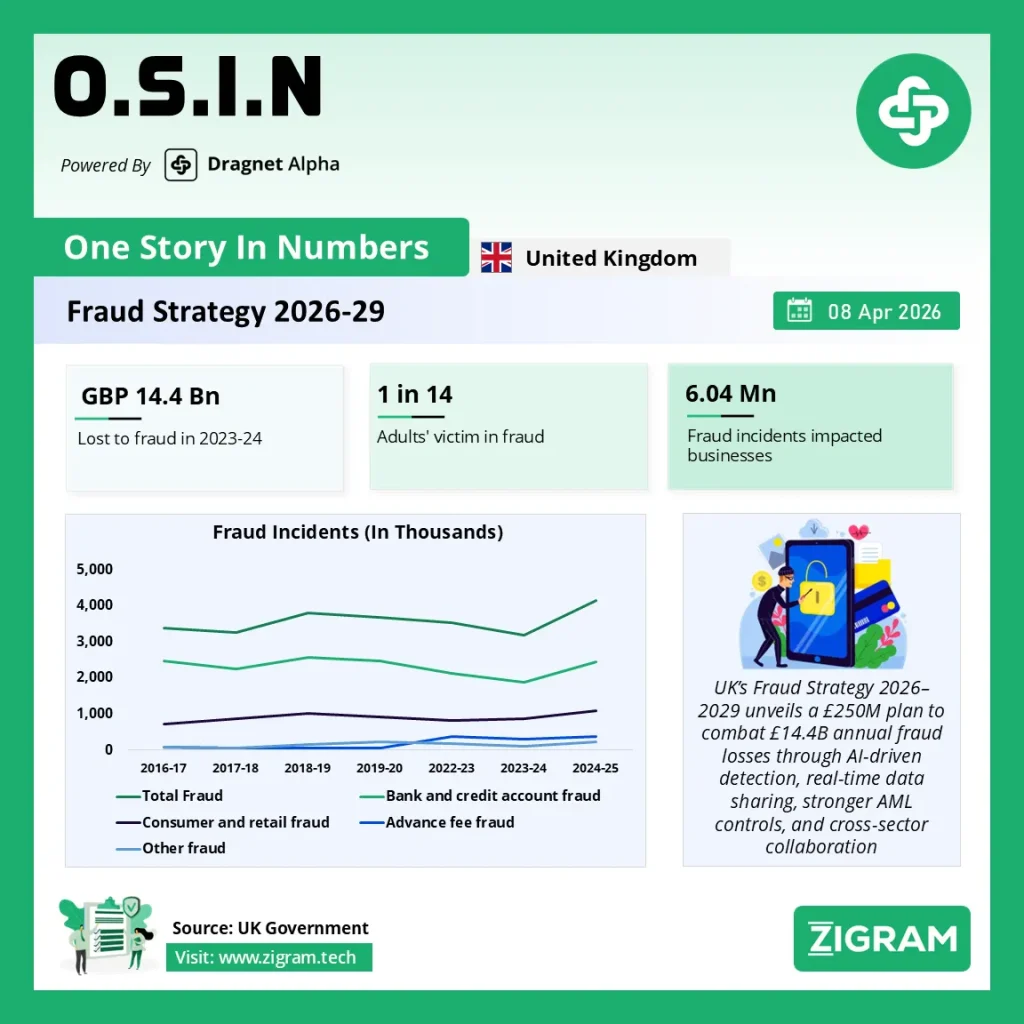

- £14.4 billion lost to fraud in 2023–2024

- 4 million fraud offences annually (year ending Sept 2025)

- Fraud accounts for 45% of all crime

- 1 in 14 adults are victims of fraud

- 1 in 4 businesses experienced fraud in the past year (~389,000 businesses)

- 6.04 million fraud incidents impacted businesses

Financial impact is only one dimension. The report reveals:

- 74% of fraud cases involve financial loss, with ~75,000 cases exceeding £10,000

- 92% of victims suffer emotional or mental harm

For AML professionals, this reinforces a key reality:

👉 Fraud is no longer downstream of AML—it is deeply interconnected with money laundering, cybercrime, and organized crime networks.

The Evolution of Fraud: Technology, Scale, and Industrialisation

The strategy identifies fraud as a technology-enabled, transnational crime.

Key Drivers:

- Industrialised Fraud Ecosystems

- Fraud is now run through scam compounds and call centres

- Linked to human trafficking, corruption, and organized crime networks

- Operates globally, often beyond jurisdictional reach

- Fraud-as-a-Service Economy

- Dark web marketplaces sell:

- Phishing kits

- Stolen credentials

- Fraud automation tools

- AI-Driven Fraud

- Use of:

- Deepfakes

- Voice cloning

- Generative AI phishing

- Platform Exploitation

- 53% of APP fraud originates via social media and communication platforms

- Crypto & Cross-Border Laundering

- Crypto increasingly used for:

- Fraud proceeds laundering

- Cross-border transfers

- Obfuscation of financial trails

The Strategic Framework: DISRUPT – SAFEGUARD – RESPOND

The UK’s approach is built on three pillars, each with direct AML implications.

- DISRUPT: Attacking Fraud at the Infrastructure Level

This pillar marks a shift from detecting fraud to preventing it at source.

Key Initiatives

Online Crime Centre (OCC)

- £31 million investment

- Launch: 2026

- Combines:

- Financial institutions

- Telecom providers

- Tech companies

- Law enforcement

Capabilities:

- Real-time data sharing

- Fraud pattern detection

- Account freezing & website takedowns

👉 For AML teams:

This signals mandatory data collaboration ecosystems, not siloed compliance.

Telecom & Digital Infrastructure Controls

- Over 1 billion fraudulent texts blocked since 2022

- Planned:

- Stronger KYC for telecom access

- Central phone number registry

- AI-driven fraud detection

Financial System Controls

- £629.3 million stolen in H1 2025 alone

- £371.8 million from unauthorised fraud

- 2.6 million bank fraud cases (+19% YoY)

Regulatory Shifts:

- Mandatory APP fraud reimbursement (88% recovery rate)

- Repeal of static Strong Customer Authentication rules

- Push toward:

- Risk-based authentication

- Passkeys (phishing-resistant login systems)

👉 AML implication:

Authentication = new frontline AML control

Crypto Regulation

- Full FCA authorization required by 2027

- Crypto firms treated like traditional financial institutions

👉 Signals convergence of crypto compliance and AML regimes

- SAFEGUARD: Building Systemic Resilience

This pillar focuses on preventing victimisation before transactions occur.

Key Measures

Behavioural Defence Systems

- Expansion of “Stop! Think Fraud” campaign

- Integration with banks, telecoms, and platforms

Data-Driven Risk Targeting

- Use of:

- Fraud hotspot modelling

- Predictive analytics

- Example:

- Operation Callback reduced fraud losses by 67%

Education & Vulnerability Reduction

- Fraud education embedded in school curriculum

- Targeting:

- Youth (high digital exposure)

- Elderly (financial exploitation risk)

👉 AML Insight:

This reflects a shift toward “pre-transaction AML”—identifying risk before money moves.

- RESPOND: Victim-Centric Enforcement & Justice

This pillar aligns fraud enforcement with AML investigation and recovery frameworks.

Key Measures

- Launch of “Report Fraud” platform (2026)

- Fraud Victims Charter (2027)

- Enhanced:

- Civil penalties

- Criminal prosecutions

- Asset recovery frameworks

👉 For AML teams:

Expect tighter integration between:

- Fraud reporting

- Suspicious Activity Reports (SARs)

- Law enforcement workflows

Corporate Transparency & AML Convergence

The strategy strongly aligns with AML/KYC reforms:

Companies House Reform

- Mandatory identity verification

- Power to:

- Remove fraudulent entities

- Share intelligence

New Corporate Offence

- “Failure to Prevent Fraud” (effective 2025)

👉 This mirrors:

- Failure to prevent bribery (UKBA)

- Failure to prevent tax evasion

Critical AML Takeaways

- Fraud = AML Risk Multiplier

Fraud is directly funding:

- Money laundering

- Terror financing

- Organized crime

- Data Sharing Will Become Mandatory

The OCC and regulatory push signal:

- End of siloed compliance

- Rise of real-time intelligence ecosystems

- KYC is Expanding Beyond Banking

Now includes:

- Telecom providers

- Social platforms

- Crypto firms

- AI is a Double-Edged Sword

- Criminals use AI for fraud

- Regulators expect AI for detection

- Prevention > Detection

The biggest shift:

👉 From transaction monitoring → to fraud prevention architecture

Final Thought: The Future of AML is Fraud-Centric

The UK Fraud Strategy 2026–2029 is not just a policy document—it is a blueprint for the future of financial crime compliance.

It clearly signals the following:

- AML frameworks must evolve into real-time, intelligence-led systems

- Fraud prevention will become a core regulatory expectation

- Collaboration across sectors is no longer optional

For AML leaders, the message is direct:

👉 If your compliance framework is not actively preventing fraud, it is already outdated.

- #FraudStrategy

- #AMLCompliance

- #FinancialCrime

- #FraudPrevention

- #RegTech

- #CyberCrime

- #MoneyLaundering

- #KYC

- #RiskManagement

- #FinCrime

- #ComplianceLeaders

- #AIinFinance

- #CryptoRegulation

- #DigitalFraud

- #EconomicCrime