Regulation Name: Bill C-12 – Strengthening Canada’s Immigration System and Borders Act

Date Of Issue: 26 Mar 2026

Region: Canada

Agency: FINTRAC

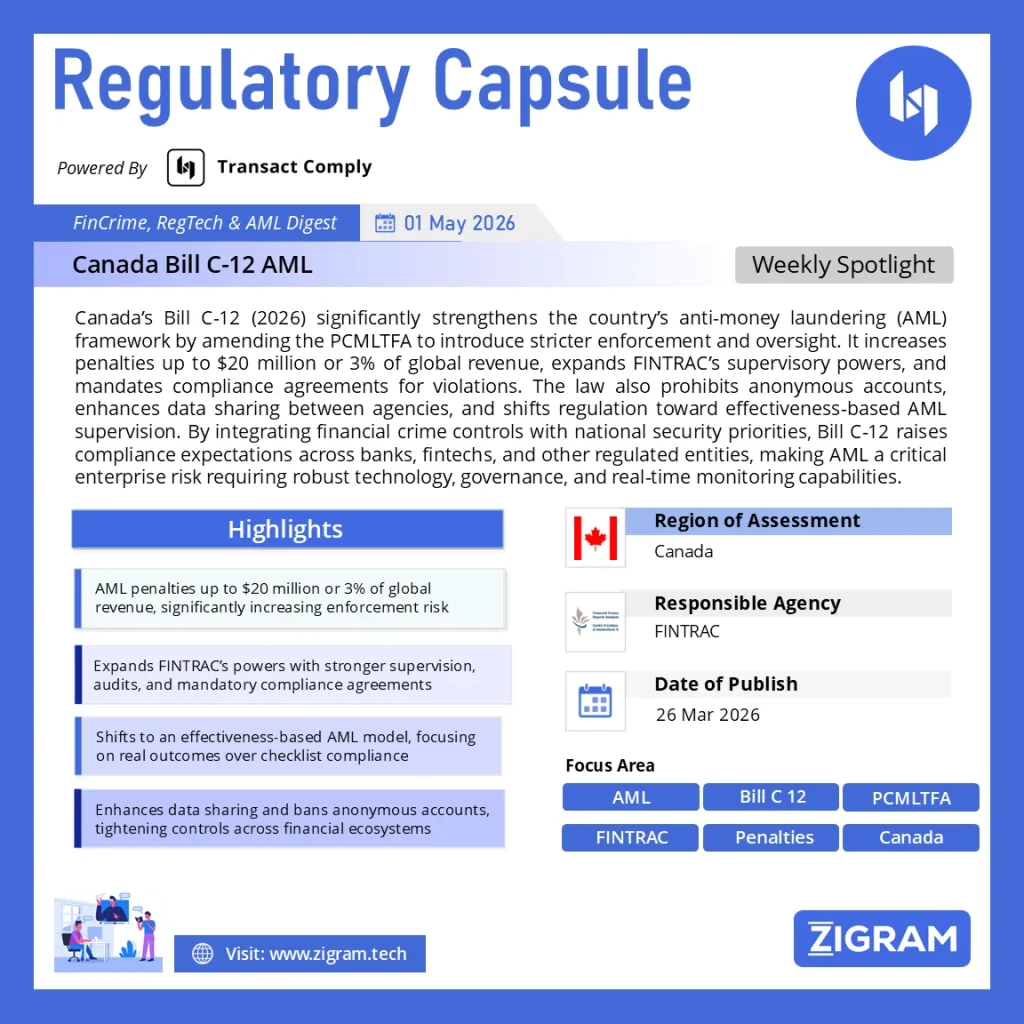

Canada Bill C-12 AML reforms, enacted on March 26, 2026, mark a significant shift in how financial crime compliance is enforced across the country. The legislation introduces sweeping amendments to the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), fundamentally changing how institutions approach risk, governance, and regulatory accountability.

For financial institutions, fintechs, and compliance leaders, Bill C-12 is not a routine regulatory update—it represents a transition toward enforcement-driven, outcome-based AML compliance, with materially higher penalties and expanded supervisory oversight.

What is Canada’s Bill C-12 AML Law?

Canada’s Bill C-12 (2026) is a major legislative reform that strengthens anti-money laundering (AML) enforcement by expanding FINTRAC’s powers, increasing penalties up to $20 million or 3% of global revenue, and introducing effectiveness-based compliance requirements under the PCMLTFA framework.

Legislative Context: AML and National Security Convergence

Bill C-12 is part of Canada’s broader strategy to address the following:

- Transnational organised crime

- Illicit financial flows

- Identity and immigration fraud

- Cross-border financial risk

This reflects a structural shift where AML is increasingly embedded within national security frameworks, rather than treated as a standalone compliance function.

For compliance teams, this means greater scrutiny, inter-agency coordination, and expanded data-sharing expectations.

Key AML Changes in Bill C-12 (2026)

- Increased AML Penalties in Canada

Bill C-12 introduces a dramatic escalation in administrative monetary penalties (AMPs):

- Minor violations: up to $40,000

- Serious violations: up to $4 million

- Very serious violations: up to $20 million or 3% of global revenue

Violation Category | Previous Max | New Max |

Minor | $1,000 | $40,000 |

Serious | $100,000 | $4 million |

Very Serious | $500,000 | $20 million |

Impact:

AML non-compliance is now a material financial risk, not just a regulatory issue.

- Expanded FINTRAC Powers

FINTRAC’s role evolves significantly under Bill C-12:

- Mandatory registration for reporting entities

- Enhanced audit and supervisory authority

- Power to enforce compliance agreements

Impact:

FINTRAC moves from an intelligence body to a proactive enforcement authority, increasing regulatory engagement frequency.

- Mandatory Compliance Agreements

Non-compliance now triggers mandatory regulatory agreements, including:

- Prescriptive remediation requirements

- Continuous monitoring obligations

- Severe penalties for breaches

Impact:

Regulatory oversight becomes ongoing rather than episodic, increasing operational pressure on compliance teams.

- Ban on Anonymous and Fictitious Accounts

Bill C-12 strengthens restrictions on:

- Anonymous financial accounts

- Fictitious identities

- Weak onboarding controls

Impact:

Organizations must upgrade KYC, identity verification, and onboarding systems, especially in digital and fintech environments.

- Shift to Effectiveness-Based AML Supervision

A key transformation is the shift toward effectiveness over formal compliance.

Regulators will now assess:

- Whether suspicious transactions are detected

- Whether controls mitigate actual risk

- Whether AML programs deliver measurable outcomes

Impact:

Checklist-driven compliance is no longer sufficient—performance and outcomes define regulatory success.

- Enhanced Data Sharing and Intelligence Integration

Bill C-12 enables broader data sharing across:

- Federal and provincial agencies

- Law enforcement bodies

- Immigration and financial intelligence systems

Impact:

Creates a connected AML ecosystem, but increases complexity around:

- Data governance

- Privacy compliance

- Cross-border data handling

- Expanded AML Scope Across Sectors

The legislation reinforces AML obligations across:

- Banks and financial institutions

- Securities dealers

- Casinos

- Fintechs and emerging platforms

Impact:

Previously under-regulated sectors now face full AML accountability and enforcement exposure.

Impact of Bill C-12 on AML Compliance Programs

- Shift to Risk-Driven AML Strategy

Organizations must move toward:

- Real-time transaction monitoring

- Advanced analytics and AI-driven detection

- Scenario optimisation and tuning

- Board-Level Accountability

With penalties tied to global revenue, AML becomes:

- A board-level risk issue

- A strategic governance priority

- Convergence of AML, Fraud, and Identity Risk

Bill C-12 connects:

- Financial crime

- Identity fraud

- Immigration risk

Implication:

Weak KYC → AML exposure → Regulatory penalties

- Increased Compliance Costs and Technology Demand

Organizations will need to invest in:

- AML technology infrastructure

- Data integration capabilities

- Skilled compliance professionals

However, cost of non-compliance far outweighs investment.

Global AML Context: Where Canada Stands

With Bill C-12, Canada aligns with global AML leaders:

- Comparable to EU AML directives in penalty severity

- More aggressive enforcement trajectory than traditional frameworks

- Moving toward centralised financial crime oversight models

This positions Canada as a high-enforcement AML jurisdiction, increasing expectations for multinational institutions.

How Compliance Leaders Should Prepare

Immediate Actions:

- Reassess enterprise AML risk frameworks

- Conduct effectiveness testing of AML programs

- Strengthen KYC and onboarding systems

- Prepare for FINTRAC audits and registration requirements

- Elevate AML governance to board level

FAQs on Canada Bill C-12 AML

What is Bill C-12 in Canada?

Bill C-12 is a 2026 law that strengthens Canada’s AML framework by increasing penalties, expanding FINTRAC’s authority, and introducing effectiveness-based compliance requirements.

How does Bill C-12 impact AML compliance?

It increases regulatory scrutiny, introduces higher penalties, and requires organizations to demonstrate that AML programs are effective—not just compliant.

What are the new AML penalties in Canada 2026?

Penalties can reach up to $20 million or 3% of global revenue, depending on the severity of violations.

Who must comply with Bill C-12?

Banks, financial institutions, fintech companies, securities dealers, casinos, and other regulated entities under the PCMLTFA.

Conclusion

Canada Bill C-12 AML reforms represent a fundamental transformation in financial crime compliance, shifting the regulatory landscape toward enforcement, accountability, and measurable effectiveness.

The implications are clear:

- Penalties are no longer manageable, they are existential

- Compliance is no longer procedural, it is performance-driven

- AML is no longer isolated, it is integrated with national security

For compliance leaders, the priority is no longer just adherence—it is building resilient, intelligence-driven AML programs that can withstand regulatory scrutiny at scale.

Read about the bill here.

Read about the product: Transact Comply

Empower your organization with ZIGRAM’s integrated RegTech solutions – Book a Demo

- #CanadaAML

- #BillC12

- #FINTRAC

- #AMLCompliance

- #FinancialCrime

- #AntiMoneyLaundering

- #RegTech

- #ComplianceLeaders

- #FintechCompliance

- #KYC

- #RiskManagement

- #GlobalAML