Table of Contents

In a world where financial transactions are increasingly digital, borderless, and instantaneous, financial data has become both an asset and a liability. The same flows that enable innovations also provide fertile ground for illicit financial activities like fraud, money laundering, terrorist financing, identity theft, and more. The theme of Global Fintech Fest 2025, “Empowering Finance for a Better World Powered by AI”, is well aligned with this challenge showing how technology can harness data not just to measure or monitor, but to take action, to fight crime, protect institutions and citizens, and ensure that finance remains a force for good.

Here, we explore how the journey from data to action works, what technologies and innovations are pushing the frontier in AML (Anti-Money Laundering) and financial crime, what the current evidence and statistics say about their effectiveness, what enablers and trade-offs exist, and what needs to happen next so that technology realises its full potential in crime-fighting.

The Challenge: Rising Threats, Rising Data, Urgent Need

Rising threat landscape

- Digital transaction volumes are surging globally, with many jurisdictions pushing toward real-time payments and mobile transactions. This increases the risk exposure because more transactions happen outside traditional banking environments or through intermediaries.

- Incidents related to fraud are growing at an alarming rate. For example, in India, between April 2024 and January 2025 there were 2.4 million digital fraud incidents amounting to losses of about ₹4,245 crore, a 67% increase from the previous year. [1]

- Criminals have increased the level of sophistication in financial crime by having synthetic identity, using deepfakes, complex layering & cross-border networks, trade-based money laundering, and use of decentralised currencies like cryptocurrencies & virtual assets.

Explosion of data

- Financial institutions, regulators, and fintechs have access to huge volumes of data such as transaction flows, customer identity / KYC / onboarding information, device and behavioural data, external information (watchlists, sanctions, adverse media), unstructured data (texts, documents) and network data (who transacts with whom, when, how much).

- Even though this raw data is accessible, it is noisy, high-volume, and often siloed. Traditional, manual or rule-based systems become overwhelmed by false positives, delayed response times, or inability to see the bigger networked picture.

Technologies & Innovations That Turn Data Into Action

To handle the complexity, volume and speed of financial crime, financial institutions and regulators are increasingly adopting advanced technologies. Below are key innovation areas:

Machine Learning (ML) and Anomaly / Behavioural Analytics

- Adaptive risk models that learn from evolving patterns, rather than fixed rule sets.

- Using behavioural analytics to capture customer behaviour over time (e.g. amounts, times, counterparties, geographies) and detect deviations.

- One report indicates AI-driven transaction monitoring systems improved detection accuracy by 36% in 2025 and reduced false positives by nearly half across leading platforms. [2]

Deep Learning, Unsupervised & Hybrid Models

- Hybrid models combine expert modules (e.g. sequence models for time patterns, anomaly detectors, auto encoders) to detect sophisticated fraud/fraudulent behaviour. For example, recent research shows models getting very high accuracy, precision, recall in synthetic / real-like datasets. [3]

- Detecting cross-border transaction anomalies is made possible using unsupervised or semi-supervised models, optimising detection rules etc. [3]

Graph Analytics & Network Detection

- Detection of patterns across relationships using graph-neural-networks or graph-based ML: Layering, circular flows of money, networks of shell companies, transaction chains.

- Innovation in privacy-preserving graph-based ML: Allowing multiple institutions to collaborate (share intelligence) without violating privacy. E.g. one recent work combined graph-based ML with fully homomorphic encryption, achieving strong predictive performance. [3]

Natural Language Processing (NLP) and Unstructured Data

- Extracting signals from unstructured sources (news, legal filings, adverse media, regulatory publications, social media) to enrich entity risk profiles.

- Automating document analysis (e.g. KYC documents, ID verification), flagging red-flags in text. According to some statistics, NLP has improved document analysis speed by 44% in 2025. [2]

Real-Time / Streaming Monitoring

- Systems are designed to handle real-time or near real-time streams of transactions so that suspicious activity can be caught as it happens rather than days or weeks later.

- The push toward cloud-based, API-driven compliance architectures allows faster and more scalable monitoring. For example, cloud AML platforms are seeing adoption and deployment across many institutions. [2]

Privacy-Preserving & Federated / Collaborative Models

- Fully Homomorphic Encryption (FHE) or Secure Multi-Party Computation (SMPC) to allow computation on encrypted data. Enables institutions or jurisdictions to share intelligence without exposing sensitive data. [3]

- Synthetic transaction datasets to enable model training and research without exposing real personal or private financial data: allow testing of detection pipelines. E.g., “AMLNet” framework that generates synthetic realistic transactions for testing detection systems. [3]

Evidence & Statistics: How Effective Are These Innovations?

Below are data points and studies that illustrate how these innovations are improving crime detection, reducing costs, improving efficiency, or expanding market investment in AML technologies.

Metric / Area | Statistic / Insight | Implications |

Market growth & investment | The global AML software market was valued at USD 2.8 billion in 2024, and is projected to reach USD 8.2 billion by 2033, growing at a CAGR of ≈ 12.6% between 2025-2033. [4] Another source estimates the AML market to be USD 4.4 billion in 2025, with projections to reach USD 22.7 billion by 2035 (CAGR ~17.8%) for the broader AML industry. [5] | Signals strong demand; institutions are investing heavily in software solutions to get ahead of regulatory and criminal risk. High growth expected over next decade; opportunity for newer tech to capture market. |

Adoption & impact on detection/false positives | AI-driven transaction monitoring systems increased detection accuracy by 36% and reduced false positives by nearly 50% in 2025. [2] | Better precision means less wasted effort by human analysts; faster/noisier alerts filtered out. |

Software vs services | In 2024 the software component of AML solutions commanded ~ 63% of revenue in the global AML market, with services growing steadily. [6] | Suggests that technology platforms are now the anchor; services support deployment, maintenance, customization. |

Geographic distribution & hottest regions | North America held ~ 29-33% of AML software market share in 2024. [4] Also, Asia-Pacific is among the fastest growing regions. [6] | Implies that regulatory pressure and digital adoption are both high in advanced economies; emerging markets are catching up rapidly. |

Solution types & dominant segments | Transaction monitoring is one of the biggest segments (≈ 35% share of AML solutions by solution type) in 2024. [7] | Shows that monitoring live flows is central; detection and alerting remain critical focus. |

Efficiency / cost / speed improvements | Use of cloud and AI in AML software has enabled faster deployment, scalability, lower latency, and often cost-savings compared to traditional on-premises/manual systems. Reports indicate cloud adoption at ~ 69% among large financial firms; AI implementation in ~ 43% in some market reports. [8] | Faster roll-outs, agility in adapting to change, and more efficient compliance operations. |

From Data to Action: Process & Enablers

Having data and good technology is essential, but turning that into crime-fighting action requires strong processes, governance, and institutional support. Below are key enablers.

Data quality, integration, and governance

- Standardisation and normalisation of data: Ensuring uniform formats, abilities to merge, map, deduce. For example, matching customer identity across systems, geographies, document formats.

- Integration across silos: Combining KYC / customer onboarding data, ongoing transactions, external intelligence (watchlists, sanctions, adverse media), device data / behavioral data, etc. Without full visibility, suspicious patterns that cross boundaries (e.g., payments + media + device anomalies) may go unseen.

- Privacy compliance: As institutions collect and process more data (including unstructured or third-party data), data protection laws (national, regional, international), customer consent, data retention policies, anonymisation / pseudonymisation become necessary.

Explainability, auditability, transparency

- When AI/ML models are used to flag suspicious behaviour, institutions must be able to explain why decisions or alerts were made: what features triggered them, whether there was bias, how false positives were handled.

- Maintaining audit trails in all workflows: when alerts occur, who reviewed them, what was the outcome, audit logs for regulatory review.

Regulatory frameworks are increasingly demanding this kind of accountability.

Human + Machine Collaboration

- Human analysts remain critical: interpreting ambiguous cases,decisions about escalation and enforcement, contextual judgment that models can’t fully capture.

- Machine tools should augment human capacity: offering ranked alerts, summarised evidence, data visualisations, suggested next steps.

- Feedback loops: human review of alerts fed back into model retraining, thresholds adjustment, typology updates.

Continuous Learning and Adaptation

- Updating typologies: criminal techniques evolve (e.g.synthetic identity, layering, cross-jurisdiction laundering, DeFi / virtual assets). Systems must incorporate new signals.

- Model retraining, monitoring model drift. Detecting when model performance degrades.

- Threat intelligence assimilation: integrating global/regional alerts, regulatory changes, government / law enforcement reports.

Collaboration & Cross-Institution / Cross-Border Data Sharing

- Sharing typologies, suspicious transaction patterns, watchlists intelligence. When one institution sees a suspicious behavior pattern, others may benefit.

- Privacy preserving collaboration (e.g. through encryption, federated learning) to allow institutions / jurisdictions / regulators to share intelligence without compromising confidentiality.

Regulatory & Policy Support

- Laws, regulations, and enforcement must keep pace: AML / CFT (Countering the Financing of Terrorism) rules, regulation of virtual assets, identity verification rules, data protection laws, cross-border cooperation.

- Incentives for adoption of advanced technologies: regulatory encouragement or requirements to deploy stronger detection; penalties for weak compliance.

- Policymaker understanding of the technological possibilities and risks (e.g. privacy, fairness, unintended exclusion).

Challenges and Future Vision in Financial Crime Prevention

Key Trade-Offs and Risks in AML and Financial Crime Detection

Even as tech advances, there are important trade-offs and risk factors to manage.

False positives, alert fatigue & resource cost

- Overly sensitive systems will generate many alerts, many of them false positives. This costs human time, reduces analyst morale, can mean real risks are missed because of overload.

- Balancing sensitivity vs specificity is hard; too conservative and criminals slip through, too aggressive and compliance teams drown in non-actionable alerts.

Bias, fairness, ethical concerns

- Models trained on past data may pick up biases (geographic, demographic, etc.). E.g. customers in certain regions or with certain digital footprints might be unfairly flagged.

- Risk of discrimination, reputational harm, regulatory liabilities.

Privacy & data protection

- Handling of personal data, especially across jurisdictions, requires compliance with data protection laws (e.g. GDPR in Europe, various national laws elsewhere).

- Use of external or open-source data, or unstructured data (e.g. social media) introduces challenges of veracity, privacy, consent.

Regulatory fragmentation & cross-jurisdiction issues

- Different jurisdictions have different AML / CFT rules, identity norms, permitted data sharing, privacy laws. Cross-border financial flows complicate detection.

- Virtual asset / cryptocurrency regulation is still uneven globally.

Resource & talent constraints

- Many institutions, especially in smaller or emerging markets, may lack data science / AI expertise, or resources (computing power, infrastructure, data engineering).

- Operationalising advanced models (deploy, monitor, maintain) is non‐trivial. It is not enough to build a prototype.

Building a Better Future: Vision & Implications

To fully realise the promise of transforming data into action for crime-fighting, several features should define the future.

- Proactive, predictive financial crime detection — systems that don’t wait for suspicious transactions to accumulate but anticipate patterns, emerging threats, detect early.

- Global coordination & interoperable standards — common frameworks for AML / CFT, shared data / typologies across jurisdictions (but consistent with privacy), ideally harmonisation in regulation for virtual assets, identity proofing etc.

- Transparent, fair, accountable AI systems — where alerts/de-cisioning processes are explainable, auditable, bias is assessed and mitigated, oversight in place.

- Inclusive detection & anti-crime — ensuring that underserved populations are not unfairly excluded or subjected to burdens because of weaker digital footprints; design solutions that work across contexts.

- Strong collaboration between industry, finance, regulators, law enforcement, technology providers — sharing threat intelligence, typologies, best practices; public-private partnerships.

- Continuous innovation & resilience — keeping up with adversarial tactics (e.g. criminals using AI, employing obfuscation, synthetic identity) and adapting technologies accordingly; ensuring systems are robust to adversarial behavior, data drift, evolving threats.

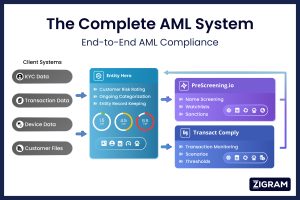

ZIGRAM: Innovation & Products Poised for Global Fintech Fest 2025

As the RegTech landscape advances, ZIGRAM is an example of a company building a suite of solutions that align with the innovations discussed — AI, real-time monitoring, inclusion, explainability, network detection, etc. At Global Fintech Fest 2025, ZIGRAM will be live on stage (in the innovation showcase) demonstrating its products, engaging with stakeholders, and showcasing how its suite converts data into actionable crime-fighting capabilities.

Key Products in ZIGRAM’s Portfolio & How They Address Innovative Crime-Fighting Needs

Based on ZIGRAM’s public product lineup, here are some of its tools and how they connect with the innovation areas.

Product / Module | Function / Description | Innovation Component | Value for Crime-Fighting / Compliance |

PreScreening.io | Name Screening (customers / third parties) for sanctions, watchlists, PEPs, adverse media, etc. | Real-time / near-real time list screening, fuzzy matching, multilingual / transliterated name variants, AI/NLP for matching inaccuracies, external unstructured data. | Helps rapidly identify risky entities before onboarding or engaging in transaction flows; reduces exposure; lowers false positives via better matching logic. |

Transact Comply | Transaction Monitoring module: real-time / scheduled monitoring of customer transactions; payment screening risk, anomalous pattern detection. | Graph analytics / network detection; anomaly detection; scenario builders; scalable architecture. | Enables detection of suspicious flows (structuring, unusual counterparty relationships, cross-account anomalies), so organisations can act more quickly, block or flag suspect transactions, and comply with AML / CFT regulations. |

Entity Hero | Systematic risk assessment of customers, including inherent + behavioral risk; dynamic scoring. | Combines multiple risk inputs, updates over time, possibly integrating external signals (sanctions, adverse media) + transactional behaviour. | Helps allocate resources: high risk vs low risk; prioritisation of due diligence; reduces burden and cost for low-risk entities; improves oversight. |

DueDiliger | Due Diligence / research driven reports to spot red flags in counterparties, entities. | Use of external data sources, document interactions, monitoring news/adverse media, possibly unstructured data analysis. | Supports deeper investigations, helps uncover hidden risks (e.g., beneficial ownership, adverse history) that may not show up in just transaction patterns. |

How ZIGRAM’s Products Embody Innovation + Inclusion + Action

From the innovations discussed earlier, ZIGRAM’s offerings align in many ways:

- Real-Time / Network / Graph Analytics: Transact Comply’s transaction monitoring, especially with pattern detection and payment screening risks, is built for real-time-ish or close to it monitoring, detecting anomalous patterns.

- Unstructured Data, NLP & Adverse Media: Name Screening, DueDiliger, and data assets like Emerging Threats / Crypto Entities draw upon external and external‐signal sources.

- Customer Risk Rating + Behavioral Signals: Entity Hero combines multiple risk dimensions and updates with behavior over time.

- Explainability / Auditability: While precise internal detail is not entirely public, the modular product design (screening, monitoring, risk scoring, due diligence) suggests separation of concerns and likely audit trails. ZIGRAM promotes low-friction but compliant tools.

- Inclusion & Accessibility: The products are described as “digital first”, scalable, low friction. This implies smaller fintechs or emerging entities can use them without huge upfront cost or complexity. Also, the focus on local / regional screening / country watchlists helps adapt to local compliance environments.

ZIGRAM’s Role at Global Fintech Fest 2025

At Global Fintech Fest 2025, ZIGRAM will be among the innovation showcases, live-demonstrating its products. Here’s what to expect:

- Live Demos: Attendees will be able to see PreScreening.io, Transact Comply, Entity Hero, DueDiliger etc. in action: how name screening works (including fuzzy matching, multilingual name issues), how transaction monitoring dashboards show anomalous patterns, how risk scoring changes with behavior, how due diligence reports help expose hidden risk.

- Interactive Sessions: Opportunities for fintechs, banks, regulators to ask questions about model thresholds, false positives, data privacy, regulatory compliance, tailoring of products to local risk environments.

- Innovation Showcase: ZIGRAM positions its “Complete AML System” — combining name screening, monitoring, risk evaluation – as a unified workflow. The showcase will demonstrate how these modules inter-operate, so that data flows smoothly from onboarding → ongoing monitoring → risk rating → enhanced due diligence.

- Engagement on Policy, Data Sharing, Responsible AI: As part of GFF conversations, ZIGRAM would engage with regulators, policy-makers, other fintechs on issues such as data privacy, transparency, avoidance of bias, emerging risks (crypto, synthetic identity, etc.).

- Customer & Fintech Enablement: For smaller actors or those new to AML compliance, ZIGRAM’s presence offers a chance to see how modular, scalable AML tools can be adopted without needing massive infrastructure or in-house data science teams.

How ZIGRAM’s Products Advance “Data → Action” Path

Linking back to the earlier sections (technologies, enablers, efficiencies), here’s how ZIGRAM helps push the financial data → action pipeline forward:

- Data acquisition & quality: ZIGRAM’s data assets (sanctions lists, country risk, crypto entity datasets, emerging threats) ensure that the input data feeding screening and scoring systems are broad, recent, and multi-sourced.

- Automated / real-time processing: Modules like Transact Comply and PreScreening.io enable faster detection; behaviour-based, pattern-based analytics reduce latency between transaction happening and alert generation.

- Ranking / Prioritisation: Entity Hero helps focus human attention on higher-risk entities, reducing the burden of reviewing all alerts; due diligence reports dig deeper only when needed.

- Explainability, Audit Trail & Regulatory Alignment: Because screening → monitoring → risk scoring → due diligence are separated but interconnected, there is clear traceability of what triggered what, which supports audits, compliance reviews, and regulatory obligations.

- Resource efficiency & inclusion: By providing scalable tools, low friction modular products, smaller fintechs or financial institutions are better able to comply, which helps broaden the net of detection and reduces risk that crime flows via under-regulated institutions.

Conclusion

ZIGRAM is a concrete example of how a RegTech entrepreneur can embody the “From Data to Action” ethos. Its product suite shows how innovations in machine learning, real-time monitoring, data assets, network / graph analytics, and risk rating are being operationalised. Likewise, its strategy to be present — live demos, interactions with regulators, showcasing unified workflows — at Global Fintech Fest 2025 reinforces the role of demonstration, collaboration, and transparency in this field.

Global Fintech Fest, with its theme “Empowering Finance for a Better World Powered by AI”, offers a platform not just for talk, but for action — where organisations like ZIGRAM show how data becomes intelligence, intelligence becomes decisions, decisions become prevention and protection.

As financial crime evolves rapidly, so must our tools, our policies, and our collaborations. ZIGRAM’s suite and approach illustrate one path forward: accessible, modular, powerful tools + data + transparent workflows. The question for the wider industry is not just can we build these tools? but can we ensure they are used responsibly, ethically, inclusively, and at scale? so finance is safe, trusted, and serves all.

Bibliography

1. From UPI to AI: The battle to safeguard India’s rapidly growing digital payments ecosystem – (ETGovernment.com)

2. Anti-Money Laundering Software Statistics 2025: Innovations and Market Growth – (CoinLaw)

3. Detecting Financial Fraud with Hybrid Deep Learning: A Mix-of-Experts Approach to Sequential and Anomalous Patterns – (arXiv)

4. Anti-Money Laundering (AML) Software Market Size, Share, Trends and Forecast by Component, Deployment Mode, Application, End Use Industry, and Region, 2025-2033 – (IMARC Group)

5. Anti-money Laundering Market Size and Share Forecast Outlook 2025 to 2035 – (Future Market Insights)

6. Anti-money Laundering Market (2025 – 2030) – (Grand View Research)

7. Anti-Money Laundering Market Evolves with AI Integration and Regulatory Advancements – (Precedence Research)

8. Top Growth Regions in the Anti-Money Laundering Software Market: Global Forecast Analysis 2025 to 2033 (360 Research Reports)

- #GENIUSAct

- #Stablecoins

- #AML

- #FinancialCrime

- #Compliance

- #CryptoRegulation

- #FinCEN

- #SanctionsCompliance

- #RegTech

- #AntiMoneyLaundering

- #DigitalAssets

- #FinancialSecurity