Table of Contents

PEP screening solutions have become a mandatory requirement for financial institutions to ensure AML compliance and reduce corruption related risks. In fact, pep screening mandatory regulations are enforced globally, making it a regulatory obligation for organizations to identify politically exposed persons (PEPs) and associated high risk individuals as part of anti money laundering aml regulations.

These requirements have been established by leading authorities such as the Financial Action Task Force (FATF), the European Union, and the Financial Crimes Enforcement Network (FinCEN). They make PEP screening a core compliance obligation for detecting high risk individuals and preventing financial crime under anti money laundering aml regulations.

With enforcement authorities issuing record penalties throughout 2025, including Monzo’s £21 million FCA fine for AML control failures and J.P. Morgan SE’s €45 million BaFin penalty, compliance teams must adopt advanced PEP screening solutions. Sanctions screening software is vital because non compliance can result in multimillion dollar fines and loss of licenses. These solutions should deliver comprehensive data coverage, minimize false positives, and integrate seamlessly with existing systems. Modern sanctions and PEP screening solutions are therefore critical for AML compliance in 2026. They help organizations meet regulatory requirements, improve automation, support real time risk detection, and ensure sanctions compliance.

This article reviews the top 5 PEP screening solutions for 2026, providing compliance leaders with insights needed to select the right software for their organizations. In addition to PEP screening, we will also touch on the top 10 sanctions screening solutions and what makes the best sanctions screening software, highlighting leading providers and essential features for regulatory adherence and operational efficiency. The best solutions combine sanctions list coverage, PEP checks, and adverse media monitoring with advanced false positive reduction technology.

Selecting the right PEP screening solution is essential. Factors such as AI capabilities, real time compliance, operational efficiency, and scalability are key to future proofing compliance programs. This guide provides a comprehensive resource to help organizations compare providers, understand regulatory requirements, evaluate features, and implement world class AML compliance strategies.

Introduction to PEP Screening Solutions

PEP screening represents a critical pillar of modern AML compliance. It serves as the frontline defense against corruption, bribery, and money laundering risks associated with individuals holding prominent public functions. The Financial Action Task Force Recommendation 12 mandates that financial institutions identify PEPs and apply enhanced due diligence. This requirement is now enforced across multiple jurisdictions, including Financial Crimes Enforcement Network (FinCEN) in the United States, the Financial Conduct Authority (FCA) in the United Kingdom, and BaFin in Germany.

The regulatory landscape has intensified significantly. Throughout 2025, enforcement actions demonstrated regulators’ diminishing tolerance for screening failures. UK law firms faced record AML fines from the Solicitors Regulation Authority for missing PEP status in property transactions. Digital banks experienced substantial penalties tied directly to weak client risk assessments and inadequate PEP identification during periods of rapid customer growth.

Advanced PEP screening solutions have become essential for operational efficiency and effective risk management. Organizations handling hundreds of thousands of customer relationships cannot rely on manual processes to identify high risk entities across multiple jurisdictions. The shift toward continuous monitoring rather than periodic batch screening reflects regulatory expectations that compliance operations must adapt in real time to changing risk profiles.

What is PEP Screening?

PEP screening is the process of identifying individuals who hold or have held prominent public positions, along with their relatives and close associates, to assess corruption and money laundering risks. As a core part of AML compliance, modern PEP screening solutions help financial institutions detect high risk individuals and apply enhanced due diligence where required.

Politically exposed persons include heads of state, senior politicians, judicial officials, military officers, executives of state owned enterprises, and officials of international organizations.

The screening process typically covers three main PEP categories:

- Foreign PEPs hold prominent roles outside the institution’s home jurisdiction and represent the highest risk category under Financial Action Task Force guidelines.

- Domestic PEPs operate within the same jurisdiction. While historically considered lower risk, current regulations increasingly require similar levels of scrutiny.

- International Organization PEPs include senior officials at institutions such as the United Nations and the World Bank.

PEP screening also extends beyond the individual. Family members such as spouses, children, parents, and siblings, as well as close business associates, may be used to hide beneficial ownership or facilitate illicit activity. This is why advanced PEP screening tools are designed to map relationships across complex ownership structures.

Modern PEP screening solutions support both real time screening during customer onboarding and ongoing monitoring of existing customers. When integrated with transaction monitoring systems, they allow institutions to detect changes across the customer lifecycle, such as when a customer becomes a PEP or when adverse media is identified.

Here is the list of Top 5 PEP Screening Solution Providers:

ZIGRAM PreScreening.io delivers the most comprehensive PEP screening and risk intelligence capabilities available in 2026, combining extensive data coverage with advanced analytics and seamless integration across the compliance platform ecosystem.

Comprehensive Global PEP Database

PreScreening.io screens against PEP databases covering 240+ jurisdictions with daily updates, ensuring compliance teams have access to current information on political appointments, departures, and status changes. The platform captures domestic PEPs, foreign PEPs, and international organization officials alongside detailed RCA mapping that extends beyond immediate family to business associates and shell company connections.

AI Powered RCA Detection and Relationship Mapping

Where many screening solutions struggle with hidden risks embedded in complex ownership structures, ZIGRAM’s advanced analytics identify RCA relationships that traditional name matching approaches miss. Graph based network analysis reveals connections across multiple entities, beneficial ownership layers, and multi generational family networks. This capability addresses one of the most significant gaps in legacy PEP screening tools.

Multilingual Screening and Advanced Matching

The platform excels in non Latin script handling, transliteration, and fuzzy matching—critical capabilities for institutions operating across multiple jurisdictions. Natural language processing reduces false positives while maintaining detection accuracy, addressing a primary operational challenge facing compliance teams globally.

Rapid Deployment and Cost Efficiency

API first architecture enables deployment in days rather than months. Cloud based and on premise options accommodate varying regulatory and infrastructure requirements. Compared to legacy enterprise solutions, ZIGRAM offers significantly lower total cost of ownership while delivering superior data coverage and operational efficiency.

ComplyAdvantage has established itself as a leading sanctions screening software provider with particular strength in serving fintech and digital native financial institutions. The platform collects PEP data in real time directly from global sources, applying machine learning to identify high risk entities and assign automated risk scoring. ComplyAdvantage specializes in real time AML data and sanctions screening, using AI driven technology to identify high risk entities.

Real Time Data and AI Driven Risk Intelligence

The platform’s PEP database updates continuously, reflecting political appointments and changes faster than many competitors relying on periodic editorial review cycles. Machine learning algorithms analyze entity relationships and contextual factors to generate risk scores that help compliance teams prioritize investigations. ComplyAdvantage offers a scalable and intelligent compliance solution powered by machine learning for PEP screening.

Developer Friendly Integration

ComplyAdvantage offers robust API capabilities designed for seamless integration with customer screening workflows, core banking systems, and onboarding platforms. For fintech companies building compliance into digital customer journeys, this developer first approach reduces implementation complexity. ComplyAdvantage is an AI driven, API first platform preferred by fintechs for real time risk intelligence.

Performance Metrics

Published case studies demonstrate strong precision. OakNorth Bank reported hit rates of approximately 2.3% for new applicant screening and 4.1% for portfolio monitoring—relatively low false positive rates indicating effective matching logic. ComplyAdvantage’s advanced AI/ML capabilities contribute to false positive reduction, improving operational efficiency for compliance teams.

Considerations

While excellent for customer screening and identity verification integration, ComplyAdvantage may require complementary solutions for comprehensive case management tools, complex compliance workflows, or deep historical data requirements. Large financial institutions with extensive RCA mapping needs should evaluate whether the platform’s graph analytics sufficiently address hidden risks in complex ownership structures.

Dow Jones Risk & Compliance provides one of the most respected PEP and adverse media databases in the industry, leveraging editorial validation processes that distinguish it from purely algorithmic competitors. The platform is trusted by large financial institutions and regulators for its data quality and contextual depth.

Manually Validated PEP Intelligence

Unlike platforms relying primarily on automated data collection, Dow Jones employs research teams to validate PEP classifications, verify RCA relationships, and contextualize risk factors. This human curated approach delivers lower false positive rates and more nuanced risk intelligence—particularly valuable for enhanced due diligence on complex cases.

Global Coverage with Contextual Depth

The platform covers PEPs across global jurisdictions with detailed profiles including appointment history, political affiliation, and associated entities. Integration with Factiva news archives enables comprehensive adverse media screening that captures reputational risks beyond regulatory lists.

Adverse Media and Risk Context

Dow Jones excels in providing narrative context around PEP relationships. Rather than simple list matching, compliance teams receive intelligence that explains why an individual qualifies as a PEP, their specific risk factors, and relevant adverse media data that informs enhanced due diligence decisions. Dow Jones Risk & Compliance leverages proprietary journalism to provide reliable adverse media screening, ensuring extensive adverse media coverage that enhances detection and compliance effectiveness.

Considerations

Premium pricing reflects the platform’s data quality, making it most suitable for institutions where screening accuracy justifies higher investment. Organizations requiring integrated transaction monitoring or case management workflows will need to combine Dow Jones Risk with third party integration platforms to achieve end to end compliance operations.

LexisNexis Risk Solutions delivers enterprise scale AML screening through its Bridger Insight XG platform, serving multinational banks and large financial institutions with complex regulatory requirements across multiple jurisdictions. LexisNexis Risk Solutions offers a suite of AML compliance tools, including watchlist screening and transaction monitoring, tailored for enterprises with complex compliance needs.

Enterprise Scale Screening Capabilities

Bridger Insight XG handles high volume batch screening and real time API checks with sophisticated name normalization across languages and character sets. The platform screens against global sanctions lists, PEP databases, and adverse media sources within a single orchestration engine. LexisNexis Risk Solutions offers robust screening with advanced analytics and strong data coverage, supporting effective false positive reduction for large scale compliance operations.

Identity Verification Integration

LexisNexis differentiates through integration with its broader identity verification and fraud detection capabilities. Institutions can combine PEP screening with identity authentication, beneficial ownership verification, and ongoing monitoring within unified compliance operations.

Visual Case Management

The platform includes visual case management tools that help analysts investigate complex relationships, document decisions, and generate audit trails satisfying regulatory expectations. LexisNexis Risk Solutions utilizes advanced AI and graph technology to reduce false positives, supporting operational efficiency. These features support the documentation requirements increasingly demanded by supervisory authorities.

Considerations

Implementation complexity and resource requirements make Bridger Insight XG best suited for organizations with dedicated compliance technology teams. Smaller institutions or those seeking rapid deployment may find the learning curve and configuration requirements challenging. Pricing reflects enterprise positioning and may not align with fintech or mid market budgets.

LexisNexis Risk Solutions integrates PEP screening as a core component of its compliance solutions, tailored for enterprises with complex compliance needs.

World Check, now part of the London Stock Exchange Group (LSEG), represents one of the most established PEP screening databases globally. Banks, insurers, and regulatory agencies have relied on World Check for decades, creating a de facto industry standard for certain compliance use cases.

Comprehensive PEP and Risk Database

World Check maintains one of the largest commercially available PEP databases, covering domestic and foreign PEPs across virtually all jurisdictions with detailed RCA mapping. Human editorial validation ensures data quality while structured risk classifications enable consistent treatment across customer portfolios.

LSEG Data Infrastructure

Backing by LSEG provides World Check with resources for continuous database expansion, regulatory research, and technology investment. Organizations requiring assurance about long term data availability and vendor stability value this institutional backing.

Batch Processing Strengths

The platform excels in periodic rescreening of large customer databases, with established integration patterns for legacy core banking systems. Institutions with mature compliance operations often have existing World Check implementations, reducing switching costs for expansions.

Considerations

World Check’s strength in batch processing may not fully address requirements for real time screening during digital onboarding. API modernization efforts continue, but institutions seeking the most agile integration capabilities may need to evaluate whether World Check’s interfaces align with their technology architecture. Premium pricing positions the platform for large financial institutions rather than emerging fintechs.

Why PEP Screening is Required for Financial Institutions

Regulatory Mandates and Global Standards

PEP screening requirements derive from binding international standards and national legislation. FATF Recommendation 12 explicitly requires that financial institutions implement measures to identify customers and beneficial owners who are PEPs, applying enhanced due diligence where such relationships exist.

The EU 4th, 5th, and 6th AML Directives mandate PEP identification and risk based treatment across all member states. The forthcoming EU AML Authority will further harmonize enforcement expectations across the bloc. In the UK, the Money Laundering Regulations 2017 (as amended) require regulated firms to maintain written policies for PEP identification and risk management. FinCEN has expanded AML/CFT obligations to investment advisers effective January 2026, extending PEP screening requirements beyond traditional banking.

Enhanced Due Diligence Obligations

Identification of PEP status triggers specific regulatory obligations. Institutions must obtain senior management approval before establishing or continuing PEP relationships. They must take reasonable measures to establish the source of wealth and source of funds involved in the business relationship. Ongoing monitoring must be conducted with increased scrutiny proportionate to the relationship’s risk profile.

These enhanced due diligence requirements apply to foreign PEPs automatically and to domestic PEPs based on risk assessment. Close associates and family members require similar treatment when the relationship presents elevated risk.

Enforcement Actions and Penalties

Recent enforcement demonstrates the financial and reputational consequences of PEP screening failures:

Monzo Bank (UK) – The FCA fined Monzo £21,091,300 in July 2025 for systemic AML control failures that included deficient customer risk assessment and PEP identification. The bank’s rapid growth from 600,000 customers in 2018 to over 5.8 million by 2022 outpaced its compliance infrastructure, demonstrating how scaling without adequate screening tools creates regulatory exposure.

J.P. Morgan SE (Germany) – BaFin imposed approximately €45 million in penalties in November 2025 for AML control failings including delayed suspicious transaction reporting—often linked to inadequate upstream screening processes.

UK Law Firms – The Solicitors Regulation Authority and Solicitors Disciplinary Tribunal issued record fines against law firms for incomplete client risk assessments and poor PEP detection in property transactions.

Beyond direct penalties, PEP screening failures create lasting reputational damage, restrictions on business activities, and increased supervisory scrutiny that burdens compliance operations for years following violations.

Essential Checklist Before Selecting Any PEP Screening Solutions

1. Assess Current Screening Gaps

Evaluate your existing PEP screening capabilities against regulatory requirements. Document instances where current processes have failed to identify PEPs, produced excessive false positives, or created operational bottlenecks. Identify whether gaps exist in RCA mapping, ongoing monitoring, or integration with customer screening workflows.

2. Define Data Coverage Requirements

Determine which jurisdictions require comprehensive coverage based on your customer base and business activities. Assess whether your solution must capture local level PEPs (municipal, regional officials) or only national figures. Evaluate RCA mapping requirements—simple family identification versus extended relationship networks.

3. Evaluate Integration Architecture

Map how PEP screening must connect with existing systems: onboarding platforms, core banking, transaction monitoring, and case management tools. Determine whether real time API integration or batch processing better suits your operational model. Assess whether the solution supports your technology stack without extensive custom development.

4. Analyze False Positive Performance

Request performance metrics from vendors including hit rates, false positive rates, and matching algorithm specifications. Solutions with poor precision create significant operational costs as analysts investigate irrelevant alerts. Compare vendor claims against published case studies and reference customer experiences

5. Verify Real Time and Batch Capabilities

Digital onboarding requires real time screening that returns decisions within seconds. Ongoing monitoring of existing portfolios may utilize batch processing. Ensure your selected solution supports both modes with appropriate update frequencies for your risk tolerance.

6. Review Audit Trail and Reporting Features

Regulators expect documented evidence of screening decisions, including rationale for dismissing alerts and escalation of confirmed matches. Verify that the solution generates comprehensive audit trails, supports regulatory reporting requirements, and provides explainability for matching logic.

7. Confirm Security and Compliance Certifications

PEP data constitutes sensitive personal information subject to GDPR, CCPA, and other data protection regulations. Verify vendor certifications including ISO 27001, SOC 2, and relevant financial services compliance standards. Assess data residency options and access controls.

8. Calculate Total Cost of Ownership

Consider licensing costs, implementation expenses, integration development, ongoing maintenance, and analyst workload from false positives. Premium solutions with lower false positive rates may deliver better value than cheaper alternatives requiring extensive manual review.

Depth of PEP Screening Required for World Class Compliance

Beyond Regulatory Minimums

World class PEP screening exceeds basic compliance requirements to provide genuine protection against corruption and reputational risks. While regulations establish minimum standards, institutions facing complex customer relationships or operating in high risk sectors must implement capabilities that identify potential risks before they create exposure.

Comprehensive RCA Identification

Effective screening must identify relationships extending beyond immediate family:

- Direct family members: spouses, children, parents, siblings

- Extended family networks: in laws, grandchildren, cousins with significant interaction

- Business associates: individuals who share beneficial ownership in legal entities, serve on boards together, or engage in significant commercial relationships

- Shell company connections: persons linked through corporate vehicles that may obscure beneficial ownership

Graph based relationship mapping technology identifies these connections across multiple data sources, revealing hidden risks that simple name matching misses.

Multi Generational Risk Assessment

PEP risk extends beyond the individual holding public office. Adult children may be used to receive corrupt payments. Spouses may hold assets acquired through illegal means. Business associates may serve as conduits for bribes. World class screening evaluates the entire network, not just the named PEP.

Continuous Monitoring and Trigger Events

One time screening at onboarding proves insufficient as customer circumstances change. Effective solutions implement continuous monitoring that detects:

- Customers who assume PEP roles after relationship establishment

- Changes in PEP status (departure from office, elevation to higher risk positions)

- Adverse media emergence regarding existing PEP relationships

- Sanctions designations affecting PEPs or associated entities

Trigger based rescreening responds to events rather than arbitrary periodic reviews, aligning with emerging regulatory expectations for perpetual KYC.

Adverse Media Integration

PEP screening must incorporate adverse media monitoring to capture reputational risks beyond regulatory lists. Negative news regarding corruption allegations, legal proceedings, human rights violations, or financial crimes provides critical context for risk assessment. Advanced solutions leverage natural language processing to analyze adverse media sources across languages and geographies.

Risk Scoring and Contextual Analysis

World class compliance requires risk scoring that considers:

- Jurisdiction risk: PEPs from high corruption countries warrant elevated scrutiny

- Role severity: heads of state present different risks than municipal officials

- Industry exposure: PEPs connected to high risk sectors (defense, energy, mining) require enhanced analysis

- Relationship proximity: direct family versus distant business associations

Key Features to Look for in a PEP Screening Solutions

Global PEP Database with Regular Updates

Comprehensive coverage requires databases spanning hundreds of jurisdictions with updates that reflect political changes rapidly. Evaluate whether updates occur daily, weekly, or monthly, and assess whether the vendor provides notification of significant changes affecting existing customer relationships.

Advanced RCA Detection Technology

Legacy name matching approaches fail to identify complex relationship networks. Leading solutions employ graph analytics, entity resolution, and network based analysis to reveal connections that would otherwise remain hidden risks in customer portfolios.

AI Powered Matching to Reduce False Positives

Fuzzy matching algorithms must handle name variations, transliterations, and aliases without generating excessive false positives. Machine learning improves matching accuracy over time, learning from analyst decisions to refine detection logic.

Real Time API Integration

Seamless integration with onboarding systems requires API capabilities that return screening results within seconds. Evaluate API documentation, sandbox environments for testing, and support for your technology stack.

Comprehensive Audit Trails

Every screening decision must be documented with clear rationale. The solution should capture which identifiers matched, confidence levels, analyst actions, and approval workflows. These audit trails satisfy regulatory expectations and support internal governance.

Multi Language Support

International operations require screening across character sets and languages. Evaluate capabilities for Arabic, Cyrillic, Chinese, and other non Latin scripts alongside transliteration handling.

Best Practices for PEP Screening Implementation

Implement Risk Based Enhanced Due Diligence

Not all PEP relationships present equal risk. Calibrate enhanced due diligence intensity based on:

- PEP category (foreign PEPs generally require highest scrutiny)

- Jurisdiction corruption indices

- Transaction patterns and relationship nature

- Adverse media presence

This risk based approach allocates compliance resources efficiently while ensuring appropriate treatment for elevated risks.

Establish Clear Escalation Procedures

Senior management must approve high risk PEP relationships before establishment. Create documented escalation paths specifying which roles can authorize different risk levels. Ensure approval decisions include written rationale that demonstrates appropriate consideration of PEP related risks.

Conduct Regular Staff Training

Compliance teams must understand PEP definitions across jurisdictions, recognize risk indicators, and apply screening tools effectively. Training should cover changes in regulatory requirements, updates to screening technology, and lessons from enforcement actions affecting peer institutions.

Maintain Ongoing Monitoring Programs

PEP screening cannot be a one time onboarding exercise. Implement ongoing monitoring that rescreens existing relationships at risk appropriate intervals and responds to trigger events. Document monitoring activities and resulting actions.

Document All Screening Decisions

Every alert whether confirmed match or false positive requires documented resolution with clear rationale. This documentation serves multiple purposes: regulatory examination response, internal audit evidence, and training material for improving screening precision.

Perform Independent Validation

Internal audit or external parties should periodically assess screening effectiveness. Testing should evaluate false positive rates, coverage gaps, data latency, and compliance with documented procedures.

PEP Screening in Customer Onboarding and KYC Workflows

Effective PEP screening begins at first customer contact and continues throughout the relationship lifecycle. Integration at the customer identification stage ensures that no relationship commences without appropriate risk assessment.

During onboarding, screening should occur automatically when customers provide identification information. For corporate customers, beneficial ownership analysis must trigger PEP screening for all individuals with significant control or ownership interests.

When screening identifies PEP status, enhanced due diligence procedures activate immediately. Compliance teams must gather additional information regarding source of wealth, nature of relationship, and expected transaction patterns. Senior management approval should occur before relationship establishment.

For lower risk PEP categories particularly domestic PEPs in jurisdictions with strong anti corruption frameworks streamlined approval workflows can maintain operational efficiency while ensuring appropriate documentation and periodic review.

Reducing False Positives in PEP Screening

False positives represent one of the most significant operational challenges in PEP screening. High false positive rates overwhelm compliance teams, create onboarding friction, and waste resources that should focus on genuine risks.

Advanced Matching Techniques

Effective solutions employ multiple matching approaches: phonetic algorithms, transliteration handling, nickname detection, and alias resolution. Combining techniques reduces both false positives and false negatives compared to single method approaches.

Entity Disambiguation

When multiple individuals share similar names, screening tools must disambiguate using secondary identifiers: dates of birth, nationalities, associated entities, and known locations. Solutions that match only on names without contextual disambiguation generate excessive false positives.

Contextual Risk Scoring

Not every name match warrants equivalent investigation. Risk scoring based on match confidence, PEP role severity, and jurisdiction risk helps prioritize alerts. Analysts address high confidence, high risk matches first while batch processing low risk alerts efficiently.

Machine Learning Refinement

Screening systems should learn from analyst decisions. When analysts consistently dismiss certain match patterns as false positives, machine learning can adjust matching logic to reduce similar alerts while maintaining detection of genuine risks.

Industries Requiring PEP Screening Compliance

Banks and Credit Institutions

Traditional banking faces the most comprehensive PEP screening requirements under global AML regulations. Retail banks, commercial lenders, and wealth management divisions must screen customers, beneficial owners, and transaction counterparties against PEP databases.

Insurance Companies and Pension Funds

Life insurance policies with significant cash values and pension products managing substantial assets require PEP screening to prevent money laundering through financial products. Many jurisdictions extend AML obligations explicitly to insurance sector participants.

Real Estate and Luxury Goods

Property transactions and high value goods purchases frequently appear in money laundering typologies. Regulatory extensions in the EU and UK require real estate agents, art dealers, and luxury goods merchants to conduct PEP screening for significant transactions.

Professional Services

Law firms, accounting practices, and tax advisors increasingly face AML obligations including PEP screening. UK enforcement against solicitors throughout 2025 demonstrates regulatory willingness to penalize professional services for screening failures.

Cryptocurrency Exchanges and Digital Assets

Virtual asset service providers must implement PEP screening equivalent to traditional financial institutions. Major enforcement actions against crypto exchanges including OKX’s $500+ million settlement and Coinbase’s €21.5 million fine confirm regulatory expectations for robust compliance operations.

Conclusion

PEP screening has evolved from a checkbox compliance exercise into a sophisticated risk intelligence capability that protects financial institutions from corruption exposure, regulatory penalties, and reputational damage. The enforcement landscape of 2025 2026 leaves no doubt that supervisory authorities expect comprehensive screening programs with documented procedures, advanced technology, and continuous monitoring.

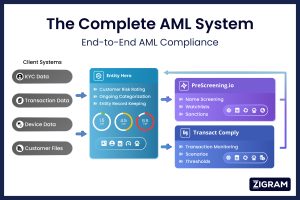

Among available solutions, ZIGRAM’s PreScreening.io delivers the most comprehensive approach to PEP screening, combining extensive global coverage with AI powered RCA detection, multilingual screening capabilities, and seamless integration across the broader compliance ecosystem. For compliance leaders seeking to reduce vendor sprawl while enhancing detection accuracy, ZIGRAM’s integrated platform addresses requirements from customer screening through transaction monitoring and case management. Together with Entity Hero, and Transact Comply, we provide “The Complete AML System“ designed to give you 100% AML compliance covering name screening, risk management, transaction monitoring, and enhanced due diligence.

The selection criteria outlined in this guide-data coverage, integration architecture, false positive performance, audit capabilities, and total cost of ownership, provide a framework for evaluating any PEP screening solution against your organization’s specific requirements.

For compliance teams navigating increasingly complex regulatory expectations, the path forward requires technology investments that deliver both accuracy and operational efficiency. The right sanctions screening solution reduces manual burden while ensuring that high risk entities receive appropriate scrutiny throughout the entire customer lifecycle.

To evaluate how ZIGRAM can strengthen your PEP screening capabilities, compliance leaders should request demonstrations that address their specific jurisdictional coverage requirements, integration needs, and operational volume expectations.