Table of Contents

Executive Overview: Why 2025 Was a Turning Point for AML ?

The Global AML Landscape 2025 was not just another enforcement cycle; it marked a structural turning point for global AML compliance. Regulators focused less on incremental guidance and more on systemic weaknesses, payment transparency, and governance accountability.

Anti-money laundering (AML) refers to the regulatory framework, policies, and technologies used to detect and prevent financial crimes such as money laundering, terrorist financing, and fraud, forming the foundation of the global AML landscape in 2025.

Payment transparency & the Travel Rule moved to centre stage: FATF agreed changes to Recommendation 16 in June 2025 to strengthen the quality of data that must travel with cross-border payments – a step with major implications for banks, payment processors and VASPs. There is also increased scrutiny on cryptocurrency exchanges for travel rule compliance.

Centralised EU supervision arrived: The European Anti-Money-Laundering Authority (AMLA) became operational mid-2025 and began work to harmonise supervision for cross-border, high-risk entities – shifting the compliance burden for pan-EU players.

Enforcement remained consequential with regional variation. Europe (notably the UK) produced large fines in 2025, while the U.S. recorded a material decline in aggregate AML/sanctions fines compared with 2024; nevertheless high-value historic cases continued to set precedents.

Taken together: “Regulators want better data, clearer governance, and demonstrable remediation. Technology and process modernization are no longer optional.”

A robust legal framework, supported by active enforcement agencies, is now central to efforts to prevent money laundering. For financial institutions, fintechs, crypto businesses, and regulated intermediaries, 2025 reset expectations around data quality, cross-border visibility, and defensible compliance architecture.

Key AML Trends 2025 at a Glance

- $1.7B US AML penalties

- £179–186M UK AML fines

- AMLA operational in the EU

- Travel Rule enforcement intensified globally

- Crypto AML scrutiny increased across jurisdictions

1. EU AML Landscape 2025: AMLA and Centralised Supervision

The biggest structural AML development of 2025 in Europe was the operational launch of the European Anti-Money-Laundering Authority (AMLA). The Anti-Money Laundering Authority (AMLA) was established in 2024 to supervise high-risk financial institutions in the EU, strengthening the legal framework for combating financial crime across EU member states.

What Changed in 2025

AMLA became operational in mid-2025, headquartered in Frankfurt.

Staffing crossed ~80 core professionals by year-end, focused on supervisory design, FIU coordination, and rulebook harmonisation.

AMLA formally began pre-supervisory risk mapping of cross-border, high-risk institutions (large banks, payment firms, crypto service providers).

The EU AML legislative package moved from law to implementation planning, including:

A single EU AML rulebook supporting the harmonization of regulatory frameworks and the establishment of a unified legal framework across EU member states

Standardised customer due diligence (CDD)

Harmonised crypto AML obligations

Why AMLA Matters Now (not just in 2028)

Although AMLA’s direct supervisory powers activate around 2028, 2025 marked the start of:

Unified supervisory expectations

Reduced national discretion

Early thematic reviews across member states

Institutions operating in multiple EU jurisdictions are now expected to demonstrate consistent AML outcomes, not country-by-country variations. International cooperation and alignment with other jurisdictions are increasingly important to ensure harmonized anti-money laundering practices and effective cross-border compliance.

EU risk signal for financial institutions' compliance teams

Fragmentation is no longer tolerated. Supervisors are aligning behind a single interpretation of “effective AML”.

ZIGRAM Recommends: Entity Hero and Transact Comply enable entity-level consistency, centralised risk scoring, and harmonised transaction monitoring – critical for AMLA-era supervision.

2.UK AML Enforcement 2025: FCA Fines and Governance Focus

The UK was one of the most aggressive AML enforcement jurisdictions in 2025, both in monetary terms and regulatory posture.

Key 2025 enforcement figures:

£179–186 million in AML-related fines issued in 2025 (up from ~£38 million in the prior comparable period)

24 FCA investigations concluded between April–November 2025

15 resulted in enforcement outcomes, reflecting a higher conversion rate

Over 100 legacy investigations closed without action to refocus on high-impact cases

Regulatory bodies often require financial institutions to implement a written AML compliance policy approved by senior management.

The regulator behind this shift: the Financial Conduct Authority (FCA). The FCA, in cooperation with law enforcement agencies, has increased enforcement actions against financial institutions and individuals involved in money laundering and related financial crimes.

FCA Enforcement Focus Areas

Weak governance and oversight

Poor customer risk assessments

Ineffective transaction monitoring

Failure to act on known red flags over multiple years

Importantly, enforcement narratives focused less on technical breaches and more on why senior management failed to intervene.

Expansion of AML supervision

In 2025, the UK government confirmed that from 2026–27, the FCA will assume AML supervisory responsibility for large parts of the legal and professional services sector – significantly expanding its reach.

UK risk signal for compliance teams

“We are no longer interested in policies – show us outcomes, escalation evidence, and board accountability.”

ZIGRAM Recommends: ZIGRAM’s unified case management, audit trails, and board-ready MIS reporting directly support FCA expectations around governance discipline.

3. US AML Trends 2025: Fewer Fines, Bigger Precedents

The US told a very different AML story in 2025.

Enforcement figures

Total AML and sanctions penalties in 2025: ~$1.7 billion

This represents a 61% decline from ~$4.3 billion in 2024

Largest single AML-related penalty in 2025:

$511 million linked to Credit Suisse legacy tax-evasion facilitation

Key agencies involved included the FinCEN and the US Department of Justice. The Financial Crimes Enforcement Network (FinCEN) is a bureau of the U.S. Department of the Treasury that issues guidance and regulations for AML compliance.

Enforcement actions in the US are shaped by foundational legislation such as the Bank Secrecy Act and the Patriot Act, which require financial institutions to implement robust AML programs and cooperate with federal agencies.

Why Enforcement Fell but Risk Didn’t

Policy shifts toward a more business-friendly enforcement stance

Reduced appetite for sector-wide crypto crackdowns

Resource and staffing constraints at regulators

However, legacy cases still resulted in large, precedent-setting settlements with:

Multi-year remediation obligations

Independent monitors

Detailed reporting requirements

Financial institutions are required to report suspicious transactions by filing Suspicious Activity Reports (SARs) when they detect suspicious activity.

In the crypto sector, the Anti-Money Laundering Act of 2020 subjected cryptocurrency exchanges to the same customer due diligence requirements as financial institutions.

US risk signal for compliance teams

Lower headline fines do not reduce individual institutional exposure especially for historic control failures.

ZIGRAM Recommends: ZIGRAM’s historical tracking and remediation auditability are particularly relevant for US institutions managing deferred prosecution agreements or consent orders.

4. AML in APAC & Middle East: Rising Regulatory Pressure

Asia in 2025 was characterised by supervisory expansion, not restraint.

India: crypto and offshore enforcement

India’s FIU targeted ~25 unregistered offshore crypto platforms offering services to Indian users.

The Financial Intelligence Unit (FIU) in India monitors and analyzes suspicious financial transactions as part of the AML framework.

The Prevention of Money Laundering Act (PMLA), enacted in 2002, was designed to combat money laundering and align India with global standards.

The Enforcement Directorate plays a key role in investigating and prosecuting money laundering cases under the PMLA.

Focus areas:

AML registration failures

Inadequate KYC

Cross-border transaction opacity

This marked a clear escalation in India’s crypto AML posture.

Hong Kong & regional banking

Indian Overseas Bank’s Hong Kong branch fined HK$8.5 million (~₹9.3 crore) for significant AML control failures.

Regulators emphasised:

Weak transaction monitoring

Poor escalation

Inadequate customer risk profiling

Middle East & broader APAC

UAE regulators imposed Dh339 million+ in AML/CFT fines across exchange houses, banks, and insurers.

Across APAC, regulators prioritised:

Beneficial ownership transparency

Dynamic KYC refresh

STR quality and timeliness

In other countries, central banks and financial intelligence units play a pivotal role in implementing AML regulations, while national risk assessments help shape AML strategies and regulatory priorities.

Asia risk signal for compliance teams

Supervisors are no longer waiting for FATF evaluations – they are enforcing ahead of them.

ZIGRAM Recommends: ZIGRAM’s PreScreening.io, for name screening, and Entity Hero, for adaptive CRR capabilities, directly address APAC’s evolving risk expectations.

AML Technology Trends 2025: The Innovation Inflection Point

2025 stands out as a watershed year for AML technology and innovation, fundamentally reshaping how financial institutions address money laundering risks. As money laundering continues to threaten the integrity of the global financial system, the demand for advanced anti money laundering solutions has never been greater. Regulatory bodies, led by the Financial Action Task Force (FATF), have intensified their expectations, urging financial institutions to adopt proactive measures and leverage cutting-edge tools to combat money laundering activities.

This year, the rapid transformation of the financial sector – driven by digital payments, cross-border transactions, and the rise of virtual assets – has exposed new vulnerabilities. In response, regulated entities are accelerating the deployment of AI-powered transaction monitoring, real-time name screening, and automated customer due diligence to detect and prevent illicit financial flows. These innovations are not just about ticking compliance boxes; they are about building resilient defenses that adapt to evolving typologies of financial crimes, including terrorist financing, tax evasion, and international organized crime.

The shift is clear: anti money laundering AML compliance is moving from manual, reactive processes to intelligent, data-driven systems capable of ongoing monitoring and rapid response to suspicious transactions. Financial institutions are now expected to demonstrate not only regulatory compliance but also the technological capabilities to address money laundering at scale – across jurisdictions, customer relationships, and transaction records.

As the global fight against illicit money intensifies, 2025 marks the point where technology became the backbone of effective AML efforts. Institutions that invest in robust compliance tools and embrace innovation are better positioned to protect the financial system, meet reporting obligations, and stay ahead of emerging risks in the ever-evolving landscape of financial crimes.

AML Compliance Strategy for 2026: Action Plan

1. Fix payment transparency now

Map data gaps in SWIFT / ISO 20022 / crypto travel rule flows

Document exception handling

2. Move from entity-based to ecosystem-based risk

Link customers, counterparties, jurisdictions, and transactions

Use dynamic, behaviour-based scoring

Ensure robust customer due diligence (CDD) and maintain up-to-date KYC records, leveraging the central KYC records registry for compliance and periodic updates

3. Make governance auditable

Board-level dashboards

Clear escalation timelines

Independent testing evidence

The AML compliance officer should oversee and implement AML compliance policies, ensuring adherence to evolving regulatory frameworks

4. Prepare for centralised supervision

EU firms: AMLA-ready harmonisation

UK firms: expanded FCA scope

APAC firms: proactive regulator engagement

Adopt perpetual KYC (pKYC), continuous monitoring, and real-time monitoring to replace traditional periodic reviews and batch processing

Integrate automated regulatory reporting features to reduce errors and response times

Address high rates of false positives in transaction alerts by deploying advanced analytics to reduce alert fatigue

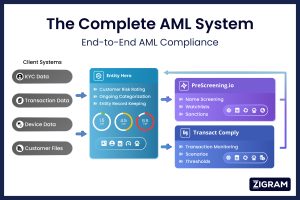

“The Complete AML System” by ZIGRAM: Entity Hero, Transact Comply, PreScreening.io, is designed precisely for this post-2025 regulatory reality with flexibility of future changes as well:

Centralised risk intelligence

Scalable transaction monitoring, name screening and risk monitoring capabilities, enhanced by artificial intelligence and agentic AI for real-time analytics, instant risk identification, and workflow automation

Modular architectures and cloud capabilities for seamless integration and deployment

Lighter, smarter, and more flexible AML solutions that scale with business needs and anticipate emerging risks

Defensible audit trails

Rapid regulatory adaptation

Conclusion: The Future of AML Compliance

2025 made one thing clear: AML is no longer about compliance coverage – it is about supervisory confidence. Institutions that can demonstrate clarity, consistency, and control will define the next era of financial crime compliance.

If you want to know where you and your company currently stand in your local and international standards, we will be happy to help you.

Book a Quick Call so we can find your pain points, explore gaps and deliver 100% AML compliance solutions.