Table of Contents

Financial crime has evolved into one of the most pressing challenges for businesses, governments, and financial institutions worldwide. As money laundering, fraud, sanctions violations, terrorist financing, and cyber-enabled financial abuse grow in sophistication, organizations are under unprecedented pressure to modernize their Financial Crime Compliance (FCC) frameworks.

In 2025, regulatory expectations are rising, global enforcement actions are intensifying, and new technologies—AI, advanced analytics, and real-time monitoring—are reshaping how companies detect, mitigate, and prevent financial crime. This article serves as a comprehensive guide to understanding financial crime, the compliance ecosystem, key global standards, and why modern RegTech solutions are essential for organisations today.

Understanding Financial Crime in 2025

In 2025, financial crime has become more complex, technology-driven, and globally interconnected than ever before. Digital banking, instant payments, cryptocurrencies, and cross-border financial services have expanded access to financial systems—but they have also created new opportunities for money laundering, fraud, sanctions evasion, and cyber-enabled abuse. At the same time, regulators worldwide are tightening AML/CFT requirements and increasing enforcement actions.

Understanding how financial crime is evolving in today’s regulatory and technological landscape is essential for organisations to build effective Financial Crime Compliance (FCC) frameworks.

What Is Financial Crime?

Financial crime refers to illegal activities that involve the movement, manipulation, or misuse of money, assets, or financial systems. Traditionally linked to fraud and money laundering, the definition has expanded significantly due to digitisation and cross-border commerce.

Common Types of Financial Crime

Financial crimes span several categories, including:

- Money laundering – concealing illicit origins of funds

- Terrorist financing – supporting extremist or violent activities

- Fraud – identity theft, credit card fraud, investment scams, cyber fraud

- Sanctions evasion – bypassing international restrictions

- Bribery and corruption

- Tax evasion

- Insider trading and market manipulation

- Proliferation financing

Each of these activities exploits loopholes in financial systems, exploiting vulnerabilities across banking, fintech, cryptocurrencies, payments, and trade services.

Financial Crime Compliance (FCC): Meaning & Importance

Financial Crime Compliance is the set of processes, controls, technologies, and governance structures organisations use to prevent, detect, and report financial crime.

It ensures institutions follow global and local AML/CFT regulations, protect customers, reduce operational risk, maintain licensing, and safeguard financial integrity.

Why does FCC matter today?

- Regulatory pressure has grown due to FATF evaluations, EU AML reforms, and U.S. FinCEN’s rule expansions

- Cybercrime and digital fraud are increasing due to online payments, open banking, and AI-driven scams.

- Cross-border financial flows make tracking illicit movements more complex.

- Reputational risk can destroy institutions that fail to maintain robust compliance programs.

- Financial institutions must maintain customer trust, especially in competitive digital markets.

Core Components of a Financial Crime Compliance Program

A strong FCC framework includes:

Customer Due Diligence (CDD) & KYC

Institutions must identify and verify customers before onboarding.

Enhanced Due Diligence (EDD) is required for high-risk customers, such as PEPs, offshore entities, and crypto-related businesses.

Transaction Monitoring

Detects unusual, suspicious, or high-risk transactions using rules-based systems, machine learning models, and behavioural analytics.

Sanctions & Watchlist Screening

- OFAC

- UN Security Council

- EU Sanctions

- Domestic regulators

- PEP lists

- Adverse media sources

- High-risk entities and jurisdictions

Suspicious Activity Reporting (SAR/STR)

Institutions must report suspicious transactions promptly, following jurisdiction-specific timelines.

Record-Keeping & Audit

Compliance teams must maintain digital logs, audit trails, and regulatory documentation.

Governance, Risk & Compliance (GRC)

Boards and senior management must oversee the compliance strategy, risk assessments, and resource allocation.

Training & Awareness

Regular training ensures staff understand typologies, red flags, and regulatory responsibilities.

Global Financial Crime Trends in 2025

- Rise of Cyber-Enabled and AI-Driven Fraud

Deepfake fraud, synthetic identity theft, account-takeover attacks, and cross-channel scams are expanding rapidly. - Regulatory Convergence Across Borders

FATF’s risk-based approach is increasingly being adopted worldwide:- EU AML Authority (AMLA)

- UK’s Economic Crime Plan

- U.S. AMLA 2020 reform

- Singapore MAS 626 updates

- UAE, Saudi Arabia, and India AML directives

- Crypto, Stablecoin & DeFi Risks

Regulators are focusing on virtual asset service providers (VASPs), requiring KYC, Travel Rule compliance, wallet monitoring, and blockchain analytics. - Beneficial Ownership Transparency

Public BO registers and global data sharing aim to reduce shell companies and trade-based money laundering. - AI & RegTech Adoption

AI-powered tools reduce false positives, speed up investigations, and integrate fragmented data sources.

Challenges Organisations Face in Financial Crime Compliance

Despite advances, compliance teams struggle with:

- Fragmented data across multiple systems

- High false positives in screening

- Manual investigations

- Evolving typologies and cross-border crime patterns

- Shortage of skilled compliance professionals

- Growing regulatory expectations

- High cost of legacy compliance infrastructure

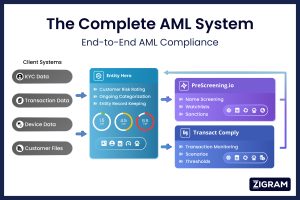

How do RegTech solutions like ZIGRAM's transform FCC?

As financial crime becomes more complex, organisations are turning to modern RegTech platforms to strengthen compliance efficiency and reduce risk.

ZIGRAM provides cutting-edge solutions that enhance screening, monitoring, risk assessment, and reporting:

- Fragmented data across multiple systems

- High false positives in screening

- Manual investigations

- Evolving typologies and cross-border crime patterns

- Shortage of skilled compliance professionals

- Growing regulatory expectations

- High cost of legacy compliance infrastructure

Automated name screening for customers, vendors, investors, and employees across:

- 3,330+ watchlists

- PEP profiles

- Vast adverse media databases

Transaction monitoring systems powered by AI and behavioural analytics.

End-to-end due diligence supported by global data, digital profiles, and risk scoring.

Intelligent risk assessment application to classify customers using customizable inputs and integrations for onboarding, monitoring, and eKYC.

ZIGRAM’s AML and FCC solutions offer:

- 15–20% lower cost

- Quick API or On-prem deployment

- High-coverage datasets

- Flexible user logins

- Pick-and-choose modular compliance suite

This makes compliance faster, smarter, and more cost-efficient—a critical advantage for banks, NBFCs, fintechs, insurers, crypto platforms, and enterprises.

The Future of Financial Crime Compliance

Over the next decade, FCC will become more integrated, automated, and intelligence-driven.

Institutions will shift from reactive compliance to predictive financial crime prevention, supported by:

- AI models that detect anomalies in real time

- Cross-border data sharing frameworks

- Unified global sanctions architecture

- Smart onboarding with digital identity

- Fully automated STR/SAR workflows

- Real-time risk scoring across entire customer journeys

The winners will be organisations that invest early in scalable, AI-based solutions.

Conclusion

Financial Crime Compliance (FCC) is the structured framework organisations use to prevent, detect, and report financial crime. Key components include KYC & Customer Due Diligence (CDD), sanctions and watchlist screening, transaction monitoring, and regulatory reporting.

As financial crime grows in complexity and global AML regulations tighten, businesses increasingly rely on advanced RegTech solutions like ZIGRAM. Tools such as DueDiliger, Entity Hero, and PreScreening.io help organisations strengthen compliance efficiency, reduce risk, and safeguard financial integrity, enabling them to stay ahead of emerging threats.

Frequently Asked Questions (FAQs)

What is Financial Crime?

Financial crime involves illegal activities that misuse, move, or conceal money or assets through financial systems. Common examples include money laundering, fraud, terrorist financing, sanctions evasion, bribery, corruption, tax evasion, and cyber-enabled scams.

What is Financial Crime Compliance (FCC)?

Financial Crime Compliance (FCC) is the set of policies, controls, and technologies organisations use to prevent, detect, and report financial crime. It includes AML programs, KYC/CDD, sanctions screening, transaction monitoring, STR/SAR filing, and governance.

Why is Financial Crime Compliance (FCC) important?

- Prevents money laundering and terrorism financing

- Protects customers and institutions from fraud

- Ensures regulatory compliance

- Reduces reputational, operational, and financial risk

- Supports safe and transparent financial systems

How RegTech Enhances Financial Crime Compliance (FCC)?

RegTech solutions like ZIGRAM improve compliance by offering:

- Automating watchlist and sanctions screening

- Using AI-powered transaction monitoring

- Providing global corporate intelligence and beneficial ownership insights

- Identifying adverse media and high-risk entities

- Accelerating onboarding and reducing false positives