Table of Contents

Complete AML System Components form the foundation of an effective anti-money laundering programme. A modern AML system is far more than a collection of compliance tools, it is an integrated architecture combining governance, KYC, sanctions screening, transaction monitoring, investigations, reporting, and risk management into a single defensible framework.

Globally, regulators from the Financial Action Task Force (established in 1989) to the agencies enforcing the Bank Secrecy Act in the U.S. now demand integrated systems that can explain how alerts lead to suspicious activity reports and decisions. A complete Anti-Money Laundering system includes policies, procedures, and technology operating as one defensible workflow. It connects customer due diligence, transaction monitoring, investigations, reporting, and recordkeeping into a single chain of evidence.

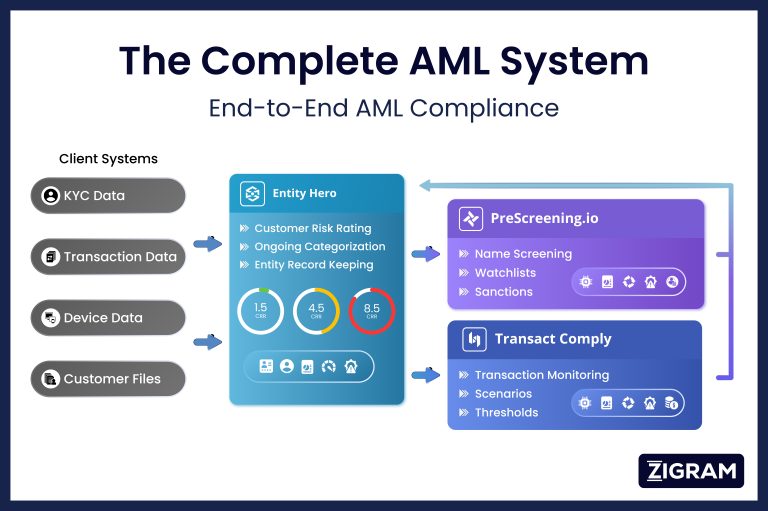

At ZIGRAM, our Complete AML System bundles name screening (PreScreening.io), transaction monitoring (Transact Comply), and entity risk assessment (Entity Hero) as the backbone of this architecture. This article walks through every key component that makes such a system work.

Get your copy of 20 Things That Make The Complete AML System here.

What are Complete AML System Components?

A complete AML system consists of governance, enterprise risk assessment, AML policies, customer due diligence (CDD), KYC, sanctions screening, adverse media monitoring, transaction monitoring, payment screening, case management, suspicious activity reporting (SAR), independent audits, data management, analytics, and ongoing monitoring. Together, these components create an end-to-end AML compliance framework that helps financial institutions detect, investigate, and prevent money laundering.

Regulatory Drivers: Why a Complete AML System Is Now Mandatory

The legal push toward integrated AML compliance has intensified over the decades:

The Bank Secrecy Act was enacted in 1970 in the U.S., creating foundational reporting and broader compliance obligations. The USA Patriot Act expanded AML requirements in 2001, mandating formal AML compliance programs with internal controls, officer designation, training, and independent testing. The Anti-Money Laundering Act of 2020 further strengthened outcome-based expectations.

The EU’s Fourth AML Directive was introduced in 2017, followed by 5AMLD (2018) and 6AMLD (2021), which expanded criminal liability to legal entities. FATF’s Forty Recommendations set global AML standards that anchor every national regime.

Enforcement trends are unmistakable: USAA Federal Savings Bank was fined $140 million for willful AML program failures, including understaffing, flawed risk scoring, and thousands of missing SARs. Coinbase paid $100 million for the KYC and transaction monitoring backlogs. Santander UK received a £107.7 million fine for systemic governance breakdowns.

Regulators no longer accept checklist compliance. They want end-to-end evidence of how data, models, a compliance officer’s judgment, and SAR filings work together.

Core Design Principles of a Complete AML System

Every component described below should reflect these principles:

Risk-based approach: controls scaled to customer, product, geography, and channel risk, aligned with FATF’s risk-based framework

Data-driven: rules, thresholds, and models calibrated using internal historical data and external typology reports

Explainable and traceable: every alert, decision, or filing is reconstructable years later during audits or enforcement actions

Cross-channel coverage: payments, trade finance, securities, insurance, and crypto transactions flowing into one AML software stack

Continuous improvement: periodic reviews, emerging risk integration, model retraining, and threshold recalibration

ZIGRAM’s Complete AML System is architected around these principles, combining configurable rules, advanced analytics, and human review into a unified workflow.

Governance, Ownership, and the Role of the Compliance Officer

Governance is the first component because without it, nothing else holds. Regulatory compliance requires clear governance structures and compliance oversight.

A formally appointed AML compliance officer (or MLRO) must be resourced, empowered, and responsible for system oversight and regulatory liaison, with adequate compliance resources across personnel, systems, and tools

Boards and senior management must approve AML policies, set risk appetite, and receive regular reporting: SAR statistics, false positive rates, backlog trends

The three lines of defence model assigns responsibilities: business units (first line), compliance and risk (second line), and internal audit (third line)

In the Santander UK case, regulators found that senior management failed to act on known weaknesses for nearly five years. In the USAA matter, key compliance roles-including the head of the Financial Intelligence Unit-sat vacant, directly causing compliance gaps. These cases demonstrate that governance failures are enforcement priorities, not afterthoughts.

ZIGRAM’s AML systems support governance with audit trails, case histories, and configurable dashboards for management and regulators.

Enterprise-Wide AML Risk Assessment

Risk assessments anchor the entire architecture. They identify vulnerabilities to money laundering and determine how intensively each area is controlled.

Periodic (at least annual) assessments must cover customers, products, services, delivery channels, and geographies

Risk assessments categorize money laundering risks with relative scores to prioritize risk levels – by customer type, geographic risks, and transaction patterns

Risk assessments must be dynamic and regularly updated; triggered by new products, jurisdictions, or emerging threats like crypto exposure or human trafficking typologies

Both internal data (transaction volumes, alerts, SARs) and external data (FATF evaluations, national risk assessments) feed the process

Risk assessment software prioritizes threats based on financial crime risks. ZIGRAM’s Entity Hero and risk-scoring engines operationalize these assessments into daily monitoring thresholds and workflows.

Policies, Procedures, and the AML Compliance Program

Written policies and procedures convert risk assessments into daily actions. AML compliance programs require internal policies, controls, and procedures. Effective AML programs consist of seven essential components spanning controls, officer designation, training, testing, CDD, monitoring, and reporting.

Core document areas include:

Customer identification and KYC

Customer due diligence (CDD) and enhanced due diligence (EDD)

Sanctions screening and watchlist procedures

Transaction monitoring rules and escalation

SAR drafting and filing timelines (generally 30 days from detection in the U.S.)

Recordkeeping and retention (5+ years under BSA and EU rules)

Training and independent testing schedules

ZIGRAM helps clients map policies directly to configurable rules, workflows, and fields in our modules, reducing the gap between what a policy says and what the technology does. Procedures must be kept current as regulations evolve – including the EU’s new AML Authority framework expected to reshape supervisory expectations.

Customer Identification, KYC, and Due Diligence

AML frameworks must include customer due diligence and KYC processes. Know Your Customer involves verifying the identity of clients, and CDD involves verifying customer identities and assessing risks. KYC processes are integral to effective customer due diligence, and regulations require CDD to prevent money laundering activities.

CIP: collecting and verifying identity documents, legal entity data, and beneficial ownership details (commonly a 25% threshold)

Standard CDD: identity verification, risk categorization, expected activity profiling

Enhanced due diligence: applies to high-risk customers such as PEPs, complex structures, sectors linked to drug trafficking, human trafficking, or narcotics corridors. EDD includes deeper source-of-wealth/source-of-funds checks, adverse media analysis, and more frequent reviews

AML software includes identity verification tools for customer authentication

Regulators punish institutions treating KYC as a checkbox exercise. Coinbase’s failure included insufficient onboarding and source-of-funds checking, directly contributing to its $100 million penalty.

ZIGRAM’s PreScreening.io and Entity Hero along with Due Diliger run KYC, risk scoring, and diligence procedures consistently at onboarding and refresh, assigning risk scores that drive downstream controls.

Sanctions, PEP, and Watchlist Screening

Watchlist screening cross-references customer data against global sanctions lists. Sanctions screening software flags entities on regulatory blacklists. This is a discrete but tightly integrated pillar of the complete AML system.

Data sets: UN, OFAC, EU, HMT/OFSI, local sanctions and law-enforcement lists, PEP and relatives/close associates (RCA) data

Timing: one-time onboarding screening plus ongoing batch/daily screening for customers, counterparties, and payments

Accuracy: fuzzy matching, transliteration handling, and de-duplication reduce false positives while catching true matches

Large banks screen tens of millions of names daily across thousands of watchlists

ZIGRAM’s PreScreening.io offers screening against 3,400+ watchlists in 70+ languages, supporting both real-time APIs and bulk workflows.

Adverse Media and ESG / Emerging Risk Intelligence

Official watchlists lag behind reality. Adverse media screening catches financial crime signals, corruption, environmental harm, sanctions evasion, and links to human trafficking or criminal exploitation before they appear on formal lists.

ESG and reputational risk factors (governance failures, environmental disasters) increasingly feed into compliance management decisions

Continuous media monitoring across multiple languages and jurisdictions provides early warning

Configurable relevance filters prevent overwhelming investigators with low-quality noise

ZIGRAM tools feed structured risk signals into the complete AML system, supporting continuous monitoring of emerging threats.

Transaction Monitoring and Behavioural Analytics

Transaction monitoring software analyzes client transaction patterns for suspicious transactions. This is where money laundering risks become visible in real activity.

Batch and real-time monitoring covers payments, deposits, withdrawals, trade finance, securities trades, and crypto transfers to detect suspicious transactions across this activity

Common scenarios: structuring/smurfing, rapid movement through multiple accounts, use of high-risk jurisdictions, unusual cash or crypto patterns, and typologies linked to human trafficking, while also helping identify potential terrorist financing patterns

Suspicious activities include unusually large cash deposits and rapid fund movements

Transaction monitoring can prevent illicit transactions from occurring

Effective transaction monitoring requires human review of alerts generated

AML technology can process millions of transactions daily

Advanced analytics layer on top of rules: machine learning models, peer grouping, outlier detection, and graph analytics uncover hidden relationships and complex schemes. AI enhances transaction monitoring and reduces false positives. Regulators now demand explainability, champion-challenger testing, and documented model governance.

ZIGRAM’s Transact Comply combines configurable rules with ML-driven risk scores and supports both cloud-native and on-premise deployments. For a deeper dive, see our transaction monitoring in AML guide.

Payment Screening and Real-Time Controls

Payment screening operates at the message level – checking SWIFT MT/MX, ISO 20022 fields against sanctions lists, embargoed countries, and high-risk counterparties before settlement.

Instant payment schemes require sub-second responses, making the balance between detection and false positives critical to customer experience

Rule sets block or hold transactions based on originator, beneficiary, bank, country, and purpose codes

Growing regulatory focus on cross-border payment transparency and travel rule implementation for virtual asset service providers (VASPs)

ZIGRAM’s AML stack integrates payment screening with case management so blocked or held payments generate reviewable alerts automatically.

Case Management, Alert Handling, and Investigations

Case management systems are used to investigate and document suspicious activity. Case management software automates the reporting of suspicious activities, turning raw alerts into structured investigations.

Core capabilities include:

Alert triage, case creation, task assignment, timeline views, and document storage

Playbooks and investigation checklists for common typologies (trade-based money laundering, mule accounts, human trafficking rings)

Integrated data views: KYC file, historical transactions, screening hits, prior SARs, and external intelligence in one screen

Audit trails capturing who did what, when, and why – including rationales for “no SAR” decisions

The Complete AML System provides a unified case manager across PreScreening.io, Transact Comply, and Entity Hero modules.

Suspicious Activity Reports, Regulatory Filings, and Escalation

AML programs help file accurate suspicious activity reports to the appropriate authorities. Financial institutions must file SARs with the Financial Crimes Enforcement Network (FinCEN) in the U.S. SARs are required for transactions indicative of criminal conduct. Suspicious Activity Reports must be filed promptly upon detection. Failure to file SARs can result in hefty fines and regulatory penalties. SARs provide critical intelligence for investigating financial crimes.

Structured templates and data pre-population from the case management system reduce errors and improve timeliness

Automated systems improve the efficiency of suspicious activity reporting

Escalation paths run from analyst to senior investigator to compliance officer or MLRO, and when review supports escalation, institutions must report suspicious transactions through the appropriate filing process

Quality expectations include narrative clarity, linkage to typologies (e.g., FATF human trafficking indicators), and consistent transaction references

Financial institutions must file suspicious activity reports for flagged transactions

A complete AML system maintains SAR logs, reference IDs, and secure access for regulators and internal audit.

Continuous Monitoring, Reviews, and Recalibration

Continuous monitoring applies to both customers and the health of the AML system itself.

Customer monitoring: periodic risk reviews, KYC refresh cycles, trigger-based reviews (address change to a high-risk country, negative news hit, unusual activity). Ongoing customer monitoring updates risk ratings based on account activity.

System performance: tracking alert volumes, conversion to cases, SAR conversion rates, false positives, investigation times, and backlog levels

Recalibration cycles: semi-annual or annual adjustments to thresholds, adding or deprecating rules, and re-training ML models based on new typologies or regulatory feedback

ZIGRAM provides configurable dashboards and analytics so compliance leaders can benchmark and optimize ongoing monitoring across jurisdictions.

Independent Testing, Audits, and Model Validation

Training and independent audits are essential for AML compliance. Independent audits test the effectiveness of the AML program. Independent audits of AML programs should occur every 12-18 months, more frequently for high-risk institutions.

Scope: policies, KYC files, transaction monitoring rules, SAR files, training records, and governance documentation

Model validation: data quality testing, back-testing, performance metrics, bias checks, and explainability documentation for any advanced analytics component

Many enforcement actions since 2019 explicitly cited poor AML model governance – USAA’s failure to validate its customer risk scoring model contributed directly to regulatory action

A complete AML system makes audits easier by centralizing logs, configurations, and historical decisions for review.

Data Architecture, Quality, and Integration

Data quality is the backbone that makes all other components viable.

A unified data model must cover customers, accounts, transactions, counterparties, documents, and unstructured content (news, PDFs)

Data quality controls: standardization, deduplication, entity resolution, and lineage tracking across source systems

Integration with core banking, payments, trading platforms, CRM, and third-party feeds via APIs and batch interfaces

Regulatory expectations for data retention span 5–7 years or more, with secure, searchable archives for investigations

ZIGRAM’s “three dimensions of data” approach ensures our modules plug cleanly into clients’ data ecosystems.

Get your copy of 20 Things That Make The Complete AML System here.

Complete AML System Technology Stack: AML Software, Advanced Analytics, and Automation

AML compliance software automates compliance tasks for financial institutions. The technology stack typically includes:

Layer | Function |

|---|---|

Screening engines | Name, sanctions, PEP matching |

Transaction monitoring | Rules + ML-based anomaly detection |

Case management | Investigation workflow and documentation |

Reporting engines | SAR/STR generation and filing |

Analytics/BI | Dashboards, KPIs, trend analysis |

Integration middleware | APIs, batch feeds, data orchestration |

Anti-money laundering software leverages machine learning for anomaly detection, alert scoring, network analysis, and investigation assistance – with emphasis on explainable outputs. In practice, it brings screening, transaction monitoring, and ongoing KYC processes into one operating environment, while automation opportunities include auto-closure of clearly low-risk alerts, pre-population of case fields, and intelligent workflow routing. AML solutions help institutions comply with global regulatory standards.

Deployment options include cloud (SaaS), on-premise, or hybrid, with considerations for data residency and scalability. ZIGRAM’s Complete AML System is a modular, API-first stack that supports practical AI while keeping human oversight central.

People, Training, and Operational Excellence

Skilled people are a core component of the AML system, not a support function. Required profiles include compliance analysts, investigators, data scientists, AML policy specialists, and system administrators.

Training is mandatory: at induction, annually, and upon role or policy changes. Topics cover typologies like human trafficking and sanctions evasion, system usage, red flags, and escalation protocols. Training and independent audits together form the assurance layer that regulators expect.

Performance management through KPIs for quality, timeliness, and consistency in investigations keeps AML teams and compliance teams operating at standard. High-profile AML failures can lead to 20-30% customer attrition, making operational excellence a business imperative beyond regulatory obligations.

ZIGRAM complements technology with managed services and expert technical assistance for investigations, data operations, and model tuning.

Deployment Models, Scalability, and Change Management

Institutions deploy complete AML systems differently depending on maturity:

Greenfield (new digital banks, fintechs): deploy an integrated stack from day one

Staged modernization (legacy banks): phased rollouts with pilot business units, parallel-run periods, and controlled migration from siloed tools

Scalability: as transaction volumes grow, new products (crypto, instant payments) launch, or new jurisdictions are added, the system must scale without architectural rework

ZIGRAM supports modular adoption, starting with PreScreening.io, then add Transact Comply and Entity Hero, and offers implementation playbooks and discovery sessions.

Measuring Effectiveness: KPIs, Dashboards, and Regulatory Outcomes

Combating money laundering requires measuring whether your system actually works, not just whether it exists.

Quantitative KPIs: alert volumes, SAR conversion rates, false-positive ratios, case handling times, backlog trends, and coverage of high-risk segments.

Qualitative measures: regulator feedback, audit findings, thematic review results, and law-enforcement outcomes (successful investigations supported by SARs).

Dashboards provide continuous visibility for compliance leaders and boards, enabling proactive tuning. When AML systems generate insights useful for fraud, credit, and enterprise risk management, the function shifts from cost centre to strategic risk intelligence – helping focus resources and reduce compliance costs while improving operational efficiency.

ZIGRAM’s analytics capabilities help clients benchmark performance across jurisdictions and business lines, helping improve operational efficiency across compliance operations.

How Complete AML System Components Work Together?

ZIGRAM’s ecosystem implements every component described above through three flagship modules:

PreScreening.io: sanctions, PEP, and adverse media screening against 3,400+ watchlists in 70+ languages

Transact Comply: rules-based and ML-enabled transaction monitoring, payment screening, and automated monitoring with integrated case and SAR management

Entity Hero: multi-factor entity risk assessment with configurable risk scores, beneficial ownership analysis, and dynamic customer data profiling

The end-to-end workflow runs from pre-onboarding screening through onboarding diligence requirements and risk scoring, into in-life transaction monitoring and continuous monitoring, through investigations, and into regulatory reporting – all with audit-ready data trails.

Typical customers include banks, fintechs, insurers, capital markets firms, and crypto platforms operating across multiple regulatory regimes. ZIGRAM’s anti-money laundering (AML) platform supports risk-based procedures that meet regulatory expectations across jurisdictions.

Conclusion: Building a Defensible, Future-Proof AML System

A complete AML system is an integrated, evolving ecosystem – not a one-time project. Its key components span governance, risk assessment, policies, KYC and due diligence, screening, transaction monitoring, case management, SARs, continuous monitoring, independent testing, data architecture, technology, and people. Each piece must connect to the next in a traceable chain that satisfies both regulatory obligations and the practical demands of preventing money laundering.

The financial services industry faces emerging threats – crypto, instant payments, online marketplaces, and sophisticated human trafficking networks – alongside tightening AML regulations and rising regulatory fines. Institutions that build integrated, risk-based AML strategies now will be the ones that pass audits, protect the financial system from criminal exploitation, and retain customer trust.

ZIGRAM is a specialist partner for institutions ready to modernize their AML procedures and compliance programs for 2026 and beyond. Book a Demo to evaluate how ZIGRAM’s Complete AML System fits your institution’s needs.

Get your copy of 20 Things That Make The Complete AML System here.