OPBAS Supervisory Report 2024-25

The Office for Professional Body Anti-Money Laundering Supervision (OPBAS) released its 2024–2025 supervisory report, providing a comprehensive assessment of Anti-Money Laundering (AML) supervision across the UK’s legal and accountancy professional body supervisors (PBSs).

The report highlights systemic supervisory weaknesses, enforcement gaps, intelligence-sharing challenges, and emerging risks, while also outlining reforms that will reshape the UK’s AML supervisory landscape.

For financial institutions, fintech companies, and compliance leaders, the report is particularly important because:

- Professional service providers (law firms, accountants, TCSPs) often act as gatekeepers to the financial system.

- Weak supervision of these sectors increases the risk of money laundering, terrorist financing, sanctions evasion, and professional enablers facilitating financial crime.

- The report signals a transition toward centralized AML supervision under the FCA, which may influence regulatory expectations across the broader financial ecosystem.

This article provides a detailed breakdown of the report’s key findings, risk indicators, enforcement trends, and strategic implications for financial institutions.

The Role of OPBAS in the UK AML Framework

OPBAS operates within the Financial Conduct Authority (FCA) and oversees 22 professional body supervisors responsible for AML supervision of legal and accountancy sectors.

These professional bodies supervise more than:

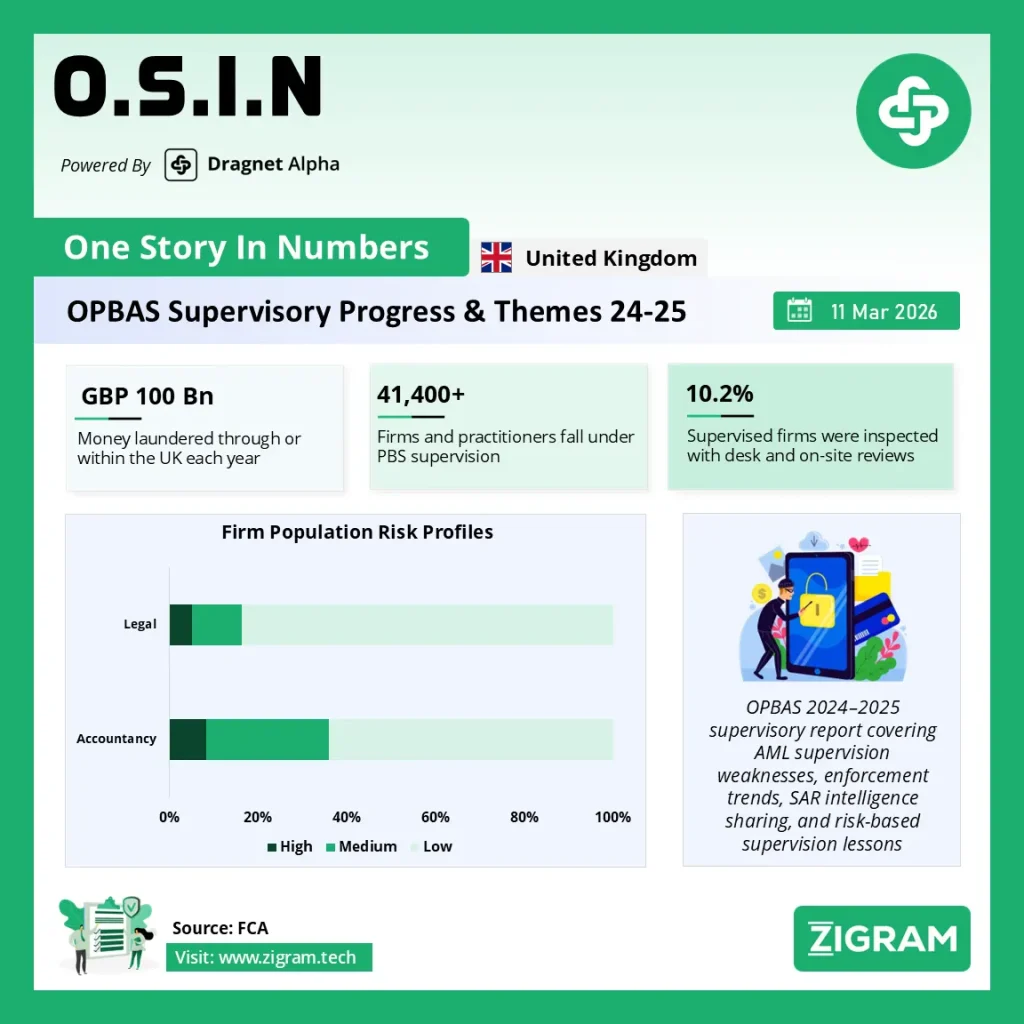

- 41,400 firms and practitioners globally

- Across sectors that contribute significantly to the UK economy

For example:

- The accountancy sector contributed £81 billion to UK GDP

- The legal sector contributed £74 billion

However, these sectors also represent major vulnerabilities in the AML ecosystem, as criminals frequently rely on professional intermediaries to:

- Establish shell companies

- Launder illicit funds

- Facilitate complex ownership structures

- Move assets across jurisdictions

According to the UK National Crime Agency, more than £100 billion may be laundered through or within the UK annually.

Key Findings from OPBAS Supervisory Assessments

Between Q4 2024 and Q1 2026, OPBAS assessed six professional body supervisors using the updated OPBAS Sourcebook methodology.

Supervisors were evaluated using four effectiveness levels:

- Effective

- Largely Effective

- Partially Effective

- Ineffective

The results reveal moderate improvement but persistent structural weaknesses, particularly in supervision and enforcement mechanisms.

Major AML Weaknesses Identified by OPBAS

- Over-Reliance on “Assisted Compliance”

One of the most significant concerns identified in the report is that some supervisors rely excessively on “assisted compliance.”

This approach focuses on helping firms correct issues rather than enforcing disciplinary actions.

The problem:

- Firms receive multiple opportunities to correct AML failures

- Enforcement action is delayed or avoided

- Deterrence against non-compliance is weakened

OPBAS warns that this approach undermines effective AML enforcement and weakens regulatory credibility.

For financial institutions, this signals potential AML risks when interacting with professional service providers, as compliance enforcement within those sectors may be inconsistent.

Persistent AML Compliance Failures

Professional firms supervised by PBSs continue to show recurring AML breaches, including:

- Inadequate Customer Due Diligence (CDD)

- Poor record keeping

- Missing or weak firm-wide risk assessments

- Poorly documented AML policies and procedures

- Incomplete client risk assessments

These failures indicate systemic compliance weaknesses across professional services.

For banks and fintech companies, this increases the risk of financial crime exposure through professional intermediaries.

Weak Enforcement Across Supervisory Bodies

OPBAS identified enforcement as one of the weakest areas of AML supervision.

Common enforcement failures include:

- Excessively long remediation timelines

- Multiple warnings before enforcement action

- Weak follow-up after remediation commitments

- Low financial penalties

For example, average fines in the accountancy sector are more than six times lower than those in the legal sector, suggesting inconsistent enforcement standards.

This enforcement disparity could create regulatory arbitrage, where high-risk actors gravitate toward weaker supervisory environments.

Risk-Based Supervision: Improvements but Key Gaps

Most professional body supervisors were rated “largely effective” in applying risk-based supervision, but several weaknesses remain.

Positive developments include:

- More structured risk assessment frameworks

- Annual data collection exercises to identify emerging threats

- Integration of intelligence sources in risk profiling

However, significant challenges remain.

Some supervisors:

- Failed to meet their own review cycles

- Used small samples for compliance reviews

- Allowed firms to select which client files were reviewed

These practices weaken the reliability of AML supervision.

Technology and AI in AML Risk Detection

The report highlights growing interest among supervisors in AI and advanced analytics to assess AML risks.

However, OPBAS warns that AI models must:

- Use reliable data

- Be fully auditable

- Be regularly tested for bias and limitations

One example cited in the report shows an AI model assigning default “medium risk” ratings to new firms due to insufficient data, meaning some firms could go two years without meaningful risk scrutiny.

For financial institutions deploying AI-driven AML solutions, this underscores the importance of model validation and continuous monitoring.

Intelligence Sharing Challenges in the AML Ecosystem

Effective AML supervision depends heavily on information sharing between regulators, supervisors, and law enforcement.

OPBAS identified several issues:

- Inconsistent use of intelligence-sharing platforms

- Varied risk appetite across supervisors

- Lack of actionable intelligence exchanges

Two key intelligence-sharing systems are central to the UK framework:

Shared Intelligence Service (SIS)

The SIS platform enables supervisors to share intelligence on AML and counter-terrorism financing risks.

In 2025 alone, SIS members recorded:

- 274 intelligence requests

- 925 intelligence uploads

However, usage varies significantly across supervisors.

Financial Crime Information Network (FIN-NET)

FIN-NET connects nearly 100 organizations including regulators, law enforcement, and financial institutions.

It allows members to:

- Share intelligence

- Coordinate investigations

- Identify emerging threats

Despite its effectiveness, referrals by professional body supervisors remain relatively low, highlighting untapped potential in cross-sector collaboration.

Suspicious Activity Reports (SARs): Quality Improving

Suspicious Activity Reports remain a critical intelligence source in the AML ecosystem.

OPBAS conducted a SAR quality review and found:

- Generally high-quality submissions

- Increasing collaboration between PBSs and the UK Financial Intelligence Unit

- Growing adoption of SAR quality reviews within supervised populations

However, the report also highlights the need for:

- Improved SAR training

- Consistent SAR review processes

- Better retention of SAR records

High-Risk Sector Spotlight: Trust and Company Service Providers (TCSPs)

Trust and Company Service Providers are a major risk vector for money laundering and terrorist financing.

TCSPs can be exploited to:

- Establish shell companies

- Obscure beneficial ownership

- Move illicit assets internationally

OPBAS continues to coordinate with regulators and supervisors to improve oversight of TCSPs.

Upcoming regulatory reforms may also expand AML obligations to include the sale of “off-the-shelf companies.”

The Future of AML Supervision in the UK

One of the most significant developments highlighted in the report is the planned transition toward a new regulatory model, where the FCA becomes the single AML supervisor for selected professional services.

This reform aims to:

- Standardize supervision

- Improve enforcement consistency

- Strengthen intelligence sharing

- Reduce fragmentation across supervisory bodies

For financial institutions, this could result in tighter regulatory oversight of professional intermediaries.

Strategic Implications for Financial Institutions

The findings of the OPBAS report have several important implications.

- Increased scrutiny of professional intermediaries

Banks should apply enhanced due diligence when onboarding:

- Law firms

- Accountancy firms

- TCSPs

- Strengthening third-party AML controls

The report warns against outsourcing AML responsibilities to technology providers without oversight, reinforcing the need for internal compliance accountability.

- Enhanced SAR intelligence collaboration

Financial institutions should increase engagement with:

- UKFIU

- Joint Money Laundering Intelligence Taskforce (JMLIT)

- Cross-sector intelligence-sharing frameworks

- Monitoring regulatory reform

The shift toward centralized supervision may change risk expectations, supervisory standards, and enforcement intensity.

Conclusion

The OPBAS 2024–2025 supervisory report provides a clear signal that while AML supervision across professional services has improved, significant structural weaknesses remain.

Key risks include:

- Weak enforcement

- Inconsistent supervision

- Poor AML compliance among professional firms

- Limited intelligence sharing

For financial institutions, these vulnerabilities underscore the importance of robust third-party risk management, enhanced due diligence on professional intermediaries, and stronger collaboration with regulators and law enforcement.

As the UK moves toward a more centralized AML supervisory model, institutions that proactively strengthen their compliance frameworks will be best positioned to manage the evolving financial crime risk landscape.

Source: OPBAS Supervisory Report 2024-25

Please read about our product: Dragnet Alpha

Click here to book a free demo

- #AML

- #CFT

- #FinancialCrime

- #SanctionsCompliance

- #ProliferationFinancing

- #TerroristFinancing

- #VirtualAssets

- #RiskBasedApproach

- #FinancialRegulation