Table of Contents

As global financial-crime risks evolve, AML onboarding has become one of the most critical defence layers for regulated institutions. Whether you are a bank, fintech, payments provider, insurer, or virtual asset service provider, your onboarding process must be strong enough to identify risky customers, meet regulatory expectations, and prevent money laundering or terrorist-financing threats.

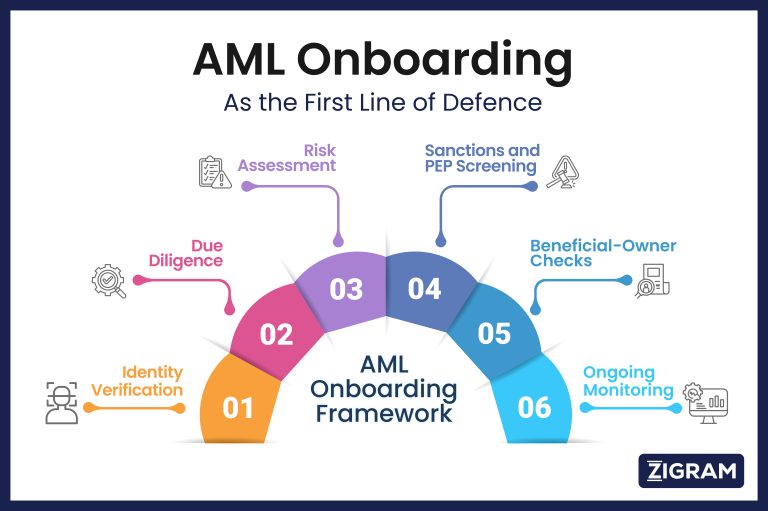

A modern AML onboarding framework integrates identity verification, due diligence, risk assessment, sanctions and PEP screening, beneficial-owner checks, and ongoing monitoring into a single connected workflow.

This guide explains the essential components, best practices, and GEO-specific considerations for an effective AML onboarding programme.

What Is AML Onboarding?

AML onboarding is the process through which organisations verify a customer’s identity, assess their money-laundering risk, and implement controls before establishing a business relationship.

Key elements include:

- Customer identification

- Document verification

- Customer Due Diligence (CDD)

- Enhanced Due Diligence (EDD) for high-risk customers

- Beneficial-ownership checks

- Sanctions, PEP, and adverse-media screening

- Risk scoring and tiering

- Ongoing monitoring

AML onboarding protects organisations from financial crime, regulatory penalties, reputational damage, and operational disruption.

Why AML Onboarding Matters

AML onboarding is the gateway to an institution’s compliance ecosystem. Weak onboarding can allow shell companies, falsified identities, sanctioned individuals, or high-risk entities to enter your system unchecked. Strong onboarding ensures:

- Regulatory compliance

- Correct risk-based customer segmentation

- Detection of financial-crime red flags

- Prevention of fraud, money laundering, and illicit flows

- Improved customer lifecycle management

- Better data for ongoing monitoring and review

Regulators worldwide expect onboarding to integrate directly with surveillance systems, reporting frameworks, and periodic reviews.

Core Components of an Effective AML Onboarding Framework

Customer Identification & Verification (CIV)

Verifying the customer’s identity is the first step in AML onboarding. This includes:

- Collecting government-issued IDs (individuals)

- Validating business registration documents (corporates)

- Verifying beneficial owners (UBOs)

- Authenticating documents through reliable sources

- Checking for inconsistencies or forged data

Identity verification forms the foundation for risk categorisation and due diligence.

Customer Due Diligence (CDD)

Customer due diligence is mandatory for all customers and involves:

- Understanding the purpose of the relationship

- Assessing expected account activity

- Identifying beneficial owners

- Reviewing source of funds or source of wealth

- Screening the customer and related parties

CDD ensures that the institution understands the customer’s background, behaviour and intent before onboarding.

Risk-Based Approach (RBA) & Risk Scoring

A risk-based approach is central to AML onboarding. Institutions should allocate resources proportionately based on risk. Common risk factors include:

- Geographical risk (high-risk jurisdictions, FATF grey/black list)

- Customer type (legal persons, trusts, NGOs, cash-intensive businesses)

- Industry/sector risk

- Product/service risk (remittance, private banking, crypto services)

- Transaction behaviour

- PEP involvement

- Adverse media exposure

After assessing these factors, the customer is given a risk score: Low, Medium or High.

Enhanced Due Diligence (EDD)

For high-risk clients, Enhanced Due Diligence (EDD) is mandatory. EDD involves:

- Additional documentation

- Verification of source of funds and source of wealth

- Deep scrutiny of UBOs

- Review of complex structures

- Senior management approval

- Detailed adverse-media analysis

- More frequent reviews

EDD strengthens compliance controls for high-risk customers.

Sanctions, PEP & Adverse Media Screening

Continuous screening is a critical control in AML onboarding. Institutions must screen:

- Customers, beneficial owners, and related entities

- Against sanctions lists, PEP databases, adverse media, enforcement, and financial-crime databases

Screening should be integrated into onboarding and ongoing monitoring.

Beneficial Ownership Identification

Understanding who truly controls a company is a regulatory expectation. AML onboarding must identify:

- Direct owners

- Indirect owners

- Ultimate beneficial owners

- Control rights and voting power

- Links to high-risk jurisdictions or entities

This prevents misuse of shell companies and complex corporate structures.

Policies, Procedures & Employee Training

A robust AML onboarding programme requires:

- Written AML/CFT policies

- Documented risk-scoring framework

- Clear escalation procedures

- Staff training

- Audit trails and record-keeping

- Internal testing and quality reviews

Policies ensure consistency; training ensures accuracy.

Technology & Automation in AML Onboarding

Modern AML onboarding demands technology-enabled solutions. Automation enables:

- Faster onboarding

- Fewer manual errors

- Digital audit trails

- Real-time screening

- Instant identity verification

- Automated case management

- Risk scoring models

- Connection to transaction monitoring

A tech-driven onboarding system improves both compliance quality and customer experience.

Ongoing Monitoring & Lifecycle Management

Onboarding is only the beginning. Post-onboarding actions include:

- Monitor transactions

- Detecting behavioural changes

- Updating risk scores

- Periodic KYC refreshes

- Investigate alerts and filing STRs

- Exiting high-risk relationships

Best Practices for AML Onboarding

✔ Apply a robust risk-based approach

Use structured scoring models and calibrate them yearly.

✔ Integrate screening at multiple points

Initial screening → UBO screening → final onboarding → ongoing screening.

✔ Automate wherever possible

Use RegTech platforms for CDD, EDD, screening, and risk scoring.

✔ Maintain an audit-ready onboarding trail

Document decisions, escalations, approvals and risk classifications.

✔ Balance compliance with user experience

Low-risk customers should have simpler onboarding paths.

✔ Align onboarding with downstream compliance

Connect onboarding decisions to monitoring, reporting and periodic reviews.

Examples of Geographic-Specific AML Onboarding Considerations

India: FIU-IND, PMLA, IFSCA rules; mandatory KYC, UBO identification, 5-year record-keeping

EU/UK: AML Directives, FCA Handbook; strict EDD on PEPs & high-risk countries

US: Bank Secrecy Act, FinCEN; strong UBO transparency, SAR filing

FATF High-Risk Jurisdictions: Enhanced screening, EDD, senior-level approvals

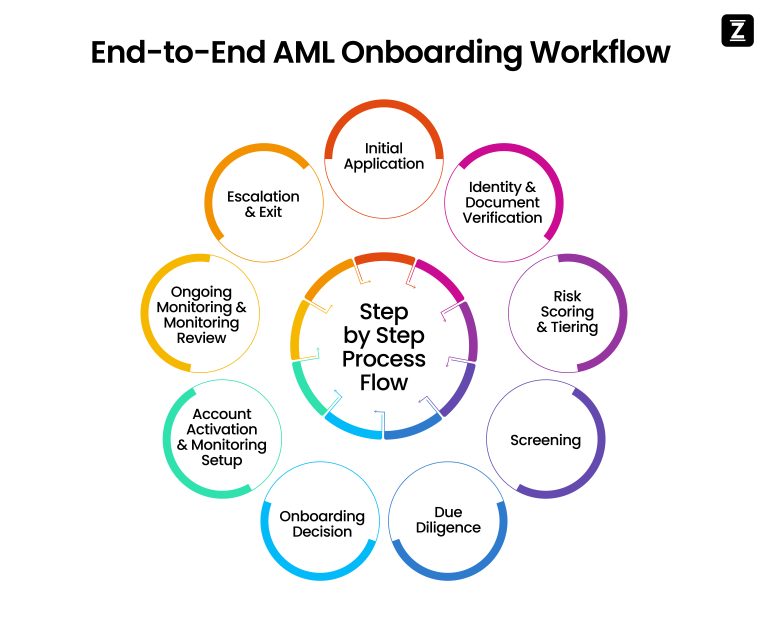

End-to-End AML Onboarding Workflow

- Initial Application: customer fills out onboarding form (identity info, business details, purpose of account).

- Identity & Document Verification: verify ID or business registration, check beneficial owners.

- Risk-Scoring & Tiering: apply risk factors (jurisdiction, business sector, transaction expectations) to assign low/medium/high risk.

- Screening: Sanctions, PEP, adverse media, beneficial-owner databases

- Due Diligence: CDD for standard-risk, EDD for high-risk

- Onboarding Decision: compliance officer approves or declines onboarding; documents risk-rating and audit-trail.

- Account Activation & Monitoring Setup: account opened with configured transaction-monitoring thresholds, alerts.

- Ongoing Monitoring & Periodic Review: periodic review of risk rating, documentation refresh, abnormal activity detection.

- Escalation & Exit: if suspicious activity occurs or risk increases (jurisdiction changes, adverse media emerges), escalate to reporting or exit relationship.

ZIGRAM delivers advanced and cost-efficient AML onboarding solutions, with:

- Global database coverage (3,330+ watchlists, extensive adverse media)

- API deployment within a week

- Flexible on-premise or cloud-based setup

- Multiple and SSO user logins

- Pick-and-choose modular architecture

- Accurate screening, faster onboarding and reduced compliance costs

Our onboarding tools help compliance teams identify risks faster, reduce operational load and meet global AML/CTF requirements.

Conclusion

AML onboarding is no longer a basic KYC formality, it is a strategic and mandatory compliance function. By combining strong due diligence, a risk-based approach, advanced screening, beneficial-ownership checks and continuous monitoring, organisations can build a resilient AML framework that protects their business and supports growth.

ZIGRAM’s RegTech solutions help businesses streamline AML onboarding, strengthen compliance and stay ahead of global regulatory expectations.

AML Onboarding: Frequently Asked Questions

What is AML onboarding?

AML onboarding is the process of verifying a customer’s identity, assessing their money-laundering risk, conducting Customer Due Diligence (CDD) or Enhanced Due Diligence (EDD), and screening against sanctions and PEP lists before establishing a business relationship.

Technology-driven solutions like ZIGRAM help automate identity verification, global screening, and risk assessment within a unified onboarding workflow.

Why is AML onboarding important?

AML onboarding prevents criminals, shell entities, and high-risk individuals from entering the financial system. It ensures regulatory compliance, reduces exposure to penalties, protects institutional reputation, and strengthens overall financial-crime risk management.

An effective onboarding framework also improves downstream monitoring and regulatory reporting accuracy.

What steps are involved in AML onboarding?

Key steps include customer identification, document verification, beneficial ownership checks, risk scoring, sanctions and PEP screening, CDD/EDD, compliance approval, and setup of ongoing monitoring throughout the customer lifecycle.

Advanced RegTech platforms like ZIGRAM streamline these steps through automated screening, risk scoring, and integrated case management.

What is Customer Due Diligence (CDD) in AML onboarding?

Customer Due Diligence (CDD) involves verifying the customer’s identity, understanding the purpose of the relationship, assessing expected transactions, identifying beneficial owners, and evaluating financial-crime risk before account activation.

CDD forms the foundation of a risk-based AML onboarding framework.

When is Enhanced Due Diligence (EDD) required?

Enhanced Due Diligence (EDD) is required for high-risk customers, such as Politically Exposed Persons (PEPs), customers from high-risk jurisdictions, or entities with complex ownership structures. It includes deeper verification, source-of-funds checks, detailed adverse-media analysis, and senior management approval.

Solutions like ZIGRAM support enhanced screening depth across global watchlists and adverse-media sources.

What is a risk-based approach (RBA) in AML onboarding?

A risk-based approach (RBA) tailors the level of due diligence based on customer risk (low, medium, or high). This ensures compliance resources are allocated efficiently while meeting regulatory expectations.

Automated risk-scoring models improve consistency and reduce manual subjectivity in onboarding decisions.

How does sanctions and PEP screening work in AML onboarding?

Customers, beneficial owners, and related parties are screened against global sanctions lists, PEP databases, enforcement lists, and adverse media sources. Screening occurs during onboarding and continues throughout the customer relationship.

ZIGRAM provides access to 3,330+ global watchlists and extensive adverse-media intelligence to support accurate, real-time screening.

How does AML onboarding connect to ongoing monitoring?

AML onboarding establishes a customer’s risk profile, which determines transaction-monitoring thresholds, review frequency, and escalation procedures. Ongoing monitoring ensures risks are identified and managed throughout the relationship.

Integrated onboarding and monitoring systems, such as those offered by ZIGRAM, help institutions maintain continuous compliance across the customer lifecycle.